HANDBOOK

Compliance First:

Why Payactiv is the EWA Leader

Last updated April 24, 2025

Table of Contents

ONE

Introduction to Payactiv

This Handbook details why Payactiv is the EWA gold standard: it is the safest, most consumer friendly EWA provider in the market, it provides two ways for users to access their earned wages for free, and it is the model preferred by the world’s largest employers.

Payactiv created earned wage access (“EWA”) in 2012 to provide workers with faster access to their earned wages. On average, American families pay $200 per month in costs associated with paycheck delay, including interest on small dollar or payday loans, credit card charges and overdraft fees. Over the years, Payactiv’s EWA solution and other livelihood benefits have saved workers millions by avoiding such costs, and by putting employees first.

As a Certified B-Corp, consumer protection is in our DNA.

As a Public Benefit Corporation and Certified B-Corp, consumer protection and social responsibility are at the heart of Payactiv’s mission. That is why the Payactiv model is the lowest cost to the user with not one but five fee-free options, relies on payroll integration for true earned wage verification, provides non-recourse factoring to protect workers, and offers transparency in deductions so that employers and employees have complete visibility. Simply put, compliance is at the core of the Payactiv platform.

TWO

The Payactiv Compliance Pledge

- Payactiv is fair to employees and safe for employers.

- Payactiv always obtains written authorization to process payroll deductions.

- Payactiv’s fees are the lowest in the industry, and we offer five free options.

- Payactiv never sells user data, and always relies on the industry’s best data security platform.

- Payactiv will not charge a user who does not use the services. Ever.

- Payactiv will indemnify and defend its clients for claims related to the Payactiv program.

Payactiv is the compliance leader, putting fairness, transparency and safety first.

We believe that all EWA programs should adhere to 3 basic principles:

- Fair to consumers

- Based on verified earned wages

- Safe for employers

Payactiv is the only EWA provider that meets these standards.

a. Payactiv is fair to consumers

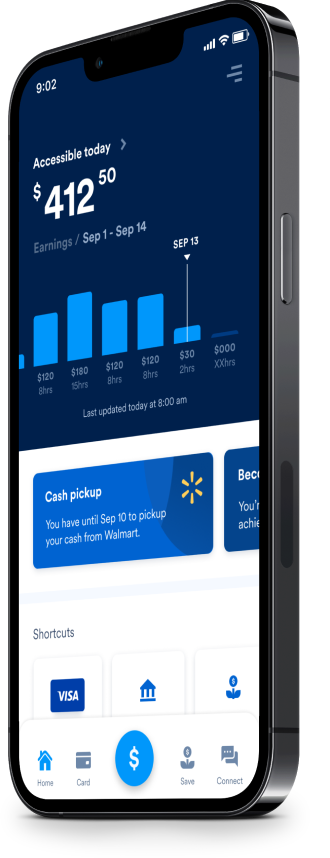

As a Certified B Corp, fairness is in our DNA. Payactiv’s standard EWA programs (including 1-3 day ACH, Uber, Amazon, and Bill Pay) are entirely free to both the user and the employer. Users with direct deposit of at least $200 to a Payactiv Card1 can also access their earned wages instantly for free. Users only pay for expedited delivery to Payactiv cards without direct deposit, third party debit cards or to pick up cash at Walmart2. The program is transparent, and Payactiv imposes no other fees (including recurring or late fees), or interest. There is no forced bank account, no credit reporting, and no collections activity.

b. Payactiv offers access to verified earned wages

Payactiv relies on payroll data to verify earnings. We do not engage in underwriting or risk decisioning, or any other lending activity.

Payactiv’s EWA program is strictly employer-based, meaning it is only available to employees of Payactiv clients. By relying on verified payroll data, Payactiv does not rely on proxy data to estimate an individual’s earnings. We see the same data the employer sees.

c. Payactiv is safe for employers

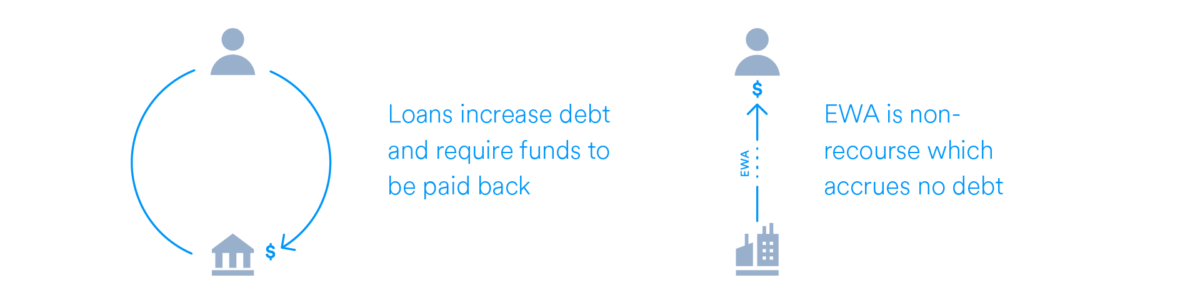

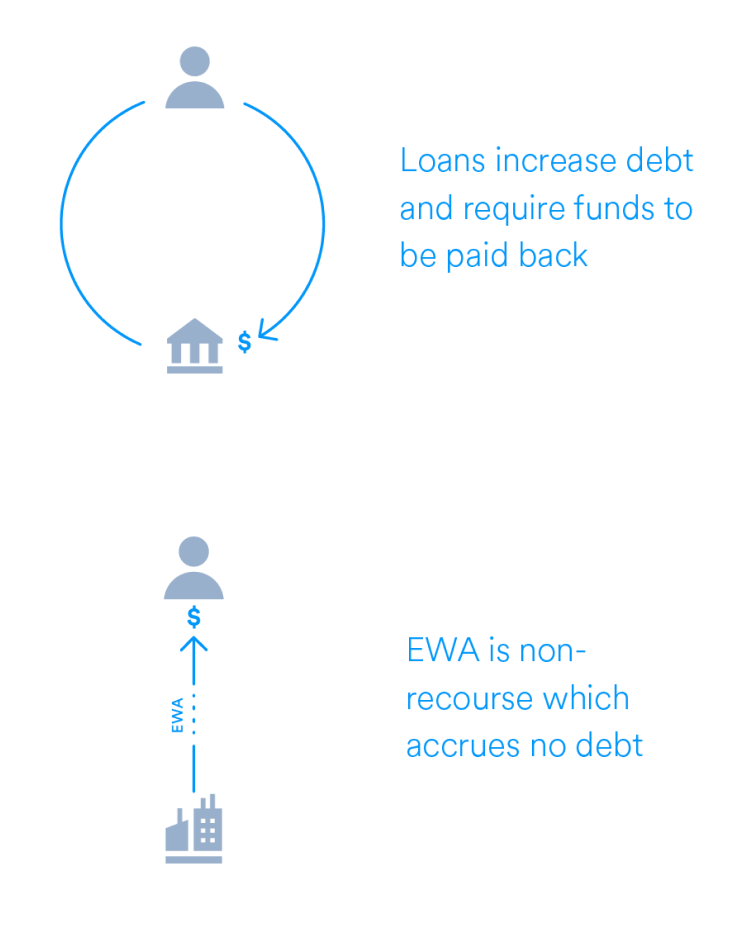

Payactiv uses factoring to purchase a receivable from the employee, meaning no debt is created and the transaction is non-recourse. Factoring is recognized in every US jurisdiction.

EWA payments are settled through a payroll deduction which promotes transparency by providing a written line-item on the user’s paystub, and Payactiv always obtains written authorization to request a deduction. Such written authorizations are recognized in all 50 states.3

THREE

Under the Hood: How Payactiv Works

a. Users download the Payactiv App and get started

Once an employer activates with Payactiv, eligible employees can download the Payactiv app for free and create a profile. Payactiv verifies the employee’s eligibility, and users agree to Payactiv’s Terms and Conditions, Privacy Policy, EFTA disclosure, and e-sign Agreement.

Once enrolled, the user gains the ability to view and access a portion of their earned wages, and utilize a number of livelihood solutions, including savings tools, messaging (depending on availability), as well as curated discounts (e.g., movie tickets, gas, prescriptions, and car insurance), financial counseling, seamless Uber and Amazon integrations, an ATM locator, and other features.

Employees can also apply for a Payactiv Visa Card directly through the app.4

Payactiv relies on payroll data directly from the employer to verify that an employee has a right to access their earned but unpaid wages owing from that employer.

Once logged in, users see an available EWA balance based on this data—usually a percentage of estimated net earned wages.5 Payactiv can also put other guardrails in place, such as limiting EWA payments to $500 per employee per pay period.6

b. Users request EWA and authorize a payroll deduction

Users can choose the amount of an EWA payment, up to the accessible balance, and may deposit these funds into the account or prepaid or debit card of their choice (including a Payactiv-branded card). In addition, through Payactiv’s embedded integrations, EWA funds can be used to pay bills, request an Uber ride, or make purchases from Amazon (all of which are free). For an optional fee, users may also request instant deposit, or obtain a cash pickup at any Walmart location.7

Payactiv always obtains written consent for a payroll deduction for the employee’s benefit.

c. The Payactiv model relies on non-recourse factoring to provide EWA

As stated in our user Terms & Conditions, Payactiv self-funds all EWA payments. The funds are provided to the user through a factoring transaction: essentially, the sale (by the employee, to Payactiv) of a present right in the future receivable representing that portion of the employee’s earned but unpaid wages. Because the employer is not a party to this private transaction, no payroll processing or wage advance requirements are triggered.

Payactiv introduced factoring to consumer EWA.

Payactiv refers to this structure as a “Factored Future Received Wage Payment,” or “FFRWP.” As discussed below, the benefit of factoring is to allow a non-recourse structure in which no debt is created between Payactiv and the user. Payactiv purchases a receivable, and obtains the right to request a deduction from the employer in the amount of that receivable. Importantly for consumer regulatory purposes, Payactiv assumes the risk associated with non-receipt of that receivable.

Payactiv’s Terms and Conditions confirm that the EWA transaction is non-recourse, does not constitute an extension of credit or create a debt, and is not an assignment of wages.

To be clear, Payactiv does not engage in underwriting, lending, “wage discounting” (the unlawful practice of charging employees to receive their paycheck), or credit reporting, and we never charge interest, recurring fees, or late fees. Payactiv unambiguously waives and disclaims any right to pursue collection or legal remedies against the user in the event of a failure to recoup EWA amounts except in the unlikely event of fraud. Payactiv has never engaged in collection activity or litigation against a user in the event of non-settlement.

d. Data and deduction file processes minimize HR and payroll burden

At the end of each pay cycle, Payactiv provides the employer with a deduction file containing the amount of the EWA and any applicable fees.8 The employer deducts EWA payments and applicable program fees from users’ paychecks and remits those funds to Payactiv pursuant to the terms of the Payactiv-employer services agreement.

Payactiv EWA transactions are easy to understand and track because each one is listed on the user’s paystub, identifies Payactiv by name, and offsets the amount already received by the employee. This gives users and payroll departments a readily-accessible written record of the transaction in the event questions arise.

Payactiv always makes its written deduction authorizations available to employer clients in the unlikely event of a dispute.

FOUR

The Industry Leader In Compliance

Payactiv’s EWA program is carefully designed to comply with consumer protection standards as well as state and federal wage and labor laws.

a. Payactiv leads the charge for legislation and regulatory clarity on employer-based EWA

Payactiv promotes a regulatory approach that recognizes EWA as a new financial product and sets basic ground rules and consumer protections applicable to all providers in the space. We support regulators throughout the country who continue to embrace responsible, payroll-based EWA business models and share Payactiv’s desire to establish basic consumer protection standards in the industry.

Most recently, the CFPB’s 2025 Advisory Opinion on EWA provides guidance that strengthens Payactiv confidence in the distinction between employer-integrated, consumer friendly EWA and other loans.9 The Opinion specifically validated that Payactiv’s service, with strong consumer protections and without the hallmarks of lending, such as interest, recourse, credit checks, or credit reporting, is not a loan and thus not controlled by lending regulations. The Opinion repeals and replaces the CFPB’s July 2024 Proposed Interpretive Rule, which had suggested treating EWA as credit but was never finalized. The Opinion, which is currently in effect, affirmatively states that covered EWA programs are not credit.

Payactiv also strongly supported Nevada’s first-in-the-country earned wage access (EWA) bill, a bipartisan effort that creates numerous consumer protections and confirms EWA is not a payday loan.10 Instead of forcing EWA into ill-fitting legacy regulatory frameworks, Nevada legislators created a new license tailored to EWA providers. In doing so, they recognize EWA as a new, innovative technology that benefits thousands of workers across the state. The legislation, which was signed on June 13, 2023, creates a number of consumer protections and differentiates between employer-integrated and direct-to-consumer providers. It ensures that EWA is non-recourse and there are no credit impacts or underwriting. The legislation also creates new protections on fees for consumers, including requiring a free option for consumers and ensuring there are no late fees, penalties, or interest in EWA transactions. Payactiv is currently licensed to provide EWA in Nevada.

Payactiv likewise supported the entry of EWA bills into law that codified a number of important consumer protections and encoded existing best practices that make EWA a pro-worker, consumer-friendly product in Arkansas, Kansas, Missouri, South Carolina, Wisconsin, and Utah.

Payactiv also engaged with California’s Department of Financial Protection and Innovation (DFPI) in developing its regulations for the earned wage access (EWA) industry and became a registered provider in California in February 2025. Payactiv’s existing service model is fully compliant with these regulations, and we are proud to continue providing our users with the EWA services they value without changes or interruptions. Payactiv continues to lead legislative and regulatory efforts on behalf of our valued clients and users who rely on EWA to achieve financial wellness and greater satisfaction at their workplace.

Summary of State Regulations and Payactiv Compliance11

| State | Date Regulations Enacted | Payactiv Compliance |

|---|---|---|

|

Arizona |

December 2022 |

AG Opinion that EWA is not a payday loan |

|

Arkansas |

March 2025 |

No licensing or registration required |

|

California |

February 2025 |

Payactiv is a registered EWA provider |

|

Connecticut |

March 2026 |

Payactiv is a licensed EWA provider |

|

Indiana |

March 2026 |

Payactiv is a licensed EWA provider |

|

Kansas |

April 2024 |

Payactiv is a licensed EWA provider |

|

Louisiana |

July 2025 |

No licensing or registration required |

|

Maine |

July 2025 |

Payactiv has an MOU with the Bureau of Consumer Credit Protection |

|

Maryland |

February 2026 |

Payactiv is a licensed EWA provider |

|

Missouri |

July 2023 |

Payactiv is a registered EWA provider |

|

Montana |

December 2023 |

AG Opinion that EWA is not a payday loan |

|

Nevada |

June 2023 |

Payactiv is a licensed EWA provider |

|

South Carolina |

May 2024 |

Payactiv is a licensed EWA provider |

|

Utah |

June 2025 |

Payactiv is a registered EWA provider |

|

Wisconsin |

April 2026 |

Payactiv is a licensed EWA provider |

Payactiv supports efforts to recognize and regulate EWA as a non-lending consumer product.

b. The Payactiv non-recourse factoring model protects users

Neither the employer nor employee are liable if there are insufficient funds to deduct on payday. On rare occasions, the EWA amount, and applicable fees, cannot be fully settled through a payroll deduction because the employee received insufficient net wages due to wage garnishment, lien, or other deductions. Payactiv’s Program Terms and Conditions provide that Payactiv may re-present such a failed deduction on subsequent paydays if necessary, but neither the employee nor the employer have any independent obligation to repay Payactiv if the attempted deduction or debit fails due to the unavailability of funds.

In addition, there is no inability-to-pay risk with Payactiv EWA transactions. Any risk an employee’s next paycheck will be insufficient to settle the EWA transaction is borne entirely by Payactiv, not the employee. Further, an employee may revoke their deduction authorization without any fee.

Payactiv relies on factoring to provide cash without a payday loan or credit.

Factoring allows one party to transfer the risk of non-payment of a receivable to another party. Payactiv introduced factoring, long a feature of commercial agreements, to EWA. By relying on factoring to provide cash to its users, Payactiv assumes the risk of nonpayment of wages, while the user obtains funds without the need for a payroll advance or payday loan. Factoring is recognized in every state, and numerous courts have held that factoring transactions are not payday loans if the funding entity has no recourse and bears the risk of loss.12

Prominent regulators agree. The Arizona Attorney General confirmed non-recourse EWA products that do not levy a “finance charge,” like Payactiv’s, are not considered consumer loans and are not subject to licensure as commercial lenders in the state.13 The Montana Attorney General also stated definitively that EWA is not a payday loan so long as the EWA product is fully nonrecourse; does not condition a transaction on any interest, fees, or other consideration or expenses; and limits transactions to income already earned by the consumer.14

c. We always obtain written authorization for payroll deductions

Payactiv obtains written consent from employees each time they perform an EWA transaction and authorize a corresponding payroll deduction. Payactiv’s deduction model not only complies with state and federal wage and labor laws, but maximizes clarity and efficiency for both the employer and employee. As discussed above, regulators and legislators both federally and on the state level have expressed a clear preference for settling EWA transactions by payroll deduction.

Payactiv relies on factoring to provide cash without a payday loan or credit.

Most states permit deductions from an employee’s wages so long as the deduction is authorized in writing. Payactiv always obtains written consent to process payroll deductions. As a result, the Payactiv model is compliant in the states that require such written consent by the employee (e.g., CA, CO, IN, KS, KY, MA, MN, MI, MO, NJ, NY, SC, VT, WI, WY).15

Other states that impose additional requirements still allow a deduction for the type of services provided by Payactiv. For example, Missouri permits deductions for “goods or services” voluntarily received by the employee “for the private benefit of the employee,”16 and Massachusetts allows deductions deemed a “valid set-off.”17 Accordingly, a voluntary deduction from an employee’s wages is allowed for the employee’s early access to those same wages. Such deductions are also permissible under the Federal Fair Labor Standards Act (“FLSA”).18

Authorized deductions for EWA transactions do not trigger wage assignment or wage discounting laws.

In general, a wage assignment occurs when the employee pledges future earnings against a present debt obligation. In other words, an assignment of wages provides collateral for an underlying loan or credit transaction, giving the lender a right to seize wages in the event of a default. Some states prohibit wage assignments because they can be associated with abusive lending practices and harmful consequences for the employee, like sacrificing an entire paycheck to cover a debt.19 These concerns are not an issue with the Payactiv model, which does not rely on a wage assignment.

Statutes governing wage assignment transactions usually focus on whether the debtor “assigns future wages to the creditor in the event of default.”20 Payactiv does not do this: we do not issue debt, deal in unearned/future wages, or most importantly, reserve recourse rights against the user.

Payactiv’s Terms & Conditions confirm these principles, and disclaim any wage assignment or debt of any kind.

“You have not assigned, transferred or conveyed your wages from employer or any part thereof. Payactiv has no right to assert a claim against you or employer with respect to your wages and has no rights, title or interest in, to or under your wages…. An FFRWP is not a credit transaction and there is no interest charged….Payactiv will not engage in any collection activity or credit reporting.” – Payactiv Terms & Conditions

Payactiv’s EWA program also does not trigger “wage discounting” laws, which generally prohibit employers from imposing conditions or obstacles which interfere with or prevent an employee from promptly receiving their due wages. To the contrary, Payactiv does just the opposite, eliminating obstacles that interfere with or prevent an employee from promptly receiving their earned wages. To be clear, Payactiv does not act as a payroll provider, and does not discharge the employer’s wage payment obligations; employees are never required to utilize the benefit or pay a fee to obtain their wages.

Employees can always receive their paycheck at no cost through the normal payroll channel.

d. Payactiv’s EWA payments do not create withholding obligations

Federal tax law requires employers to withhold certain items from employees’ wages and comply with other income tax requirements when they pay their employees. The employer’s withholdings obligations are not triggered by Payactiv’s EWA program because Payactiv does not disburse wages themselves to EWA recipients. Instead, Payactiv purchases a right to a future receivable from the employee, and, in exchange, the employee receives the value of the future receivable — the EWA amount. As for the employer, it is not a party to this factoring transaction between Payactiv and the employee, nor is the employer advancing unearned wages, which the IRS has treated as taxable compensation, for services yet to be performed by the employee.

On payday, the entire wage payment is calculated by the employer and disbursed: Payactiv collects a portion of the wage payment through a deduction file submitted to the employer pursuant to Payactiv’s agreements with both the employer and the employee (end-user). From the employer’s perspective, withholdings are calculated based on the entire wage payment amount as normal, including any amount disbursed to Payactiv. The earlier EWA payment does not involve an employment relationship and is not an actual payment of wages.

Accordingly, the employer is not required to process withholdings any differently with Payactiv.

e. Our commitment to privacy and data security

Payactiv’s commitment to compliance is further bolstered by its dedication to securing employee information. Using state of the art technology, Payactiv adheres to the strictest possible data security standards in order to safeguard employee information—and by extension—employee privacy. Payactiv maintains the following certifications, which can be made available by request:

- SOC1/SOC2 (Type 2)

- ISO27001

- PCI DSS

- CCPA Compliance Validation

f. We indemnify our clients for claims related to the Payactiv Program

Unlike most providers, Payactiv stands by every aspect of its Program and backs up its claims with contractual indemnification for its employer clients. We will indemnify clients for all claims related to the normal operation of the services, which include EWA transactions, the resulting deductions, and compliance with related state and federal law. Clients can rest easy knowing that Payactiv provides a safety-net for any claims related to the program, however unlikely.

g. The Payactiv Program avoids the compliance pitfalls of other models

Payactiv sets itself further apart from other providers by avoiding potentially drastic compliance risks. Other providers recoup EWA funds by debiting an employee’s bank account using ACH debit—which can trigger overdrafts and NSF fees—and others force the employee to open a separate “for-benefit-of” or “FBO” bank account where the employee must deposit 100% of their wages as a pre-requisite to participate in an EWA program, even if they do not use it.

FBO accounts give the provider 100% control over both the account and the employee’s paycheck, and create unique compliance risks like wage assignments.21 In addition, the net amount displayed on the worker’s paystub does not match the amount deposited in the user’s personal bank account on payday. Employees must therefore discover any errors themselves, without the benefit of a statement. And payroll departments also have no record of the amount of any EWA transaction either. This can cause unnecessary confusion for the employer and employee, as well as for lenders or others who may need to rely on employee bank statements to verify income for other reasons.

By contrast, Payactiv’s EWA offering is a true consumer-friendly, non-recourse transaction. We are guided by what is best for the employee—the worker always comes first, and always has the right to receive their unpaid, earned wages directly from the employer.

h. The Harvard Study: Payactiv Provides An Unparalleled Employee Benefit

Academic analyses of Payactiv’s EWA product have shown it provides benefits to employees for minimal cost, particularly when compared to credit-based alternatives. A 2018 paper from the Harvard Kennedy School Mossavar-Rahmani Center for Business and Government, which studied Payactiv, found that EWA programs like Payactiv’s “are more efficient than market alternatives and provide clear and compelling benefits to employees.”22

Summarizing the study, the Harvard Business Review wrote that Payactiv’s advantage is “straightforward,” since the low fee for Payactiv’s service is well below the typical $35 overdraft fee and the $30 most payday lenders charge for a two-week $200 loan. For companies offering Payactiv, turnover was found to be 19% lower among active users than among employees who enrolled but used the offering once or not at all, resulting in potential savings to employers by reducing turnover among their ranks.

Baker and Kumar, who led the Harvard study, believe that all pay “will one day be instantaneous.” “These fintech tools won’t solve America’s income disparity, but they can help people on the margins who are currently being exploited by the existing financial system,” Baker says. “And it’s in employers’ interests as well—a rare win-win.”

Our clients agree. Jaime Donnelly, Chief Financial Officer of Integrity Staffing Solutions, was interviewed by the Harvard Business Review in connection with the Payactiv study and article. Integrity offers recruiting and temporary staffing solutions to retailers across the US, and Donnelly stated that the company had seen “an uptick in attendance and a decrease in attrition” with Payactiv. She said that “Roughly 30% of our associates have signed up for the Payactiv app—we pay somewhere between 5,000 and 25,000 employees in a given week—and some $12 million in early wages have been accessed through the program.”

Payactiv protects employees and is in employers’ interests as well—a rare win-win.

FIVE

Compliance is Our Commitment

As a Public Benefit Corporation and Certified B-Corp, and the principled leader in EWA, Payactiv is unmatched in its commitment to the end-user and in its support for employer clients. We hope this Handbook helps answer any questions you have regarding Payactiv’s compliance approach and philosophy. We look forward to having you as our long-term partner.

For more information: [email protected]

The materials available in this document are for informational purposes only and not for the purpose of providing legal advice. You should contact your attorney to obtain advice with respect to any particular issue or problem.

Endnotes

- The Payactiv Visa Prepaid Card is issued by Central Bank of Kansas City, Member FDIC, pursuant to a license from Visa U.S.A. Inc. Certain fees, terms, and conditions are associated with the approval, maintenance, and use of the Card. Users should consult their Cardholder Agreement and the Fee Schedule at payactiv.com/card411. If users have questions regarding the Card or such fees, terms, and conditions, they can contact us toll-free at 877-747-5862, 24 hours a day, 7 days a week.

- Disbursement options may vary depending on location.

- Other models that require workers to divert entire paychecks as collateral for EWA payments, or which rely on underwriting to estimate earnings, may run afoul of these laws.

- Availability of the Payactiv card may vary by employer and location.

- Accessible balance is generally 50% of estimated net wages, which Payactiv calculates as 80%-90% of gross pay depending on the circumstances. Using 90% as the basis, for example, an employee with $500 in gross earned wages would have an accessible balance of $225 ([$500 x .9] /2). These rules can be customized by Payactiv and the employer.

- Other models allow employees access to 100% of their paycheck, which can produce $0 paydays, and what those providers refer to as an “over-advancement.”

- Disbursement options may vary by location.

- In three states and Puerto Rico, Payactiv debits any fees separately from the employee’s debit card via merchant debit (does not trigger overdrafts), and does not include fees in the deduction file in those states.

- Consumer Financial Protection Bureau, Advisory Opinion No. 2025-23735: Truth in Lending (Regulation Z); Non-application to Earned Wage Access Products, December 23, 2025, Federal Register, Vol. No. 90, Pg. 60069, available at https://files.

consumerfinance.gov/f/ documents/cfpb_earned-wage- access-advisory-opinion_2025- 12.pdf - Payactiv, Inc., June 15, 2023, In Watershed Moment, Nevada Enacts First EWA Bill and Confirms EWA Is Not a Payday Loan, available at https://www.payactiv.com/blog/in-watershed-moment-nevada-enacts-first-ewa-bill-and-confirms-ewa-is-not-a-loan/

- State of Arizona, Attorney General Opinion by Mark Brnovich, Attorney General, December 16, 2022, No. I22-005 (R22-011), Re: Earned Wage Access Products, available at https://www.azag.gov/

opinions/i22-005-r22-011; Payactiv, Inc., Arkansas Becomes Seventh State to Enact EWA Oversight Framework, March 21, 2025, https://www.payactiv. com/blog/arkansas-becomes- seventh-state-to-enact-ewa- oversight-framework/; Payactiv, Inc., Payactiv Becomes Registered Provider in California, March 17, 2025, https://www.payactiv. com/blog/payactiv-becomes- registered-provider-in- california/; Payactiv, Inc., Payactiv Becomes Licensed Earned Wage Access Provider in Connecticut, March 23, 2026, https://www.payactiv. com/press/payactiv-becomes- licensed-earned-wage-access- provider-in-connecticut/; Payactiv, Inc., Payactiv Becomes Licensed EWA Provider in Indiana, March 31, 2026, https://www.payactiv.com/press/payactiv-becomes-licensed-ewa-provider-in-indiana/; Payactiv, Inc., Democrat Governor Laura Kelly Signs Kansas EWA Bill into Law, April 23, 2024,https://www.payactiv.com/ blog/democrat-governor-laura- kelly-signs-kansas-ewa-bill- into-law/; Payactiv, Inc., Louisiana Becomes Eleventh State to Enact EWA Regulations, July 2, 2025, https://www.payactiv. com/blog/louisiana-becomes- eleventh-state-to-enact-ewa- regulations/; Payactiv, Inc., Payactiv Signs MOU with the State of Maine Bureau of Consumer Credit Protection, July 22, 2025, https://www.payactiv. com/blog/payactiv-signs-mou- with-the-state-of-maine- bureau-of-consumer-credit- protection/; Payactiv., Inc., Payactiv Becomes a Licensed Earned Wage Access Provider in Maryland, February 6, 2026, https://www.payactiv. com/blog/payactiv-becomes-a- licensed-earned-wage-access- provider-in-maryland/; Payactiv, Inc., Enactment of Historic Missouri Bill Shows Momentum for EWA Registration, July 7, 2023, https://www.payactiv. com/blog/enactment-of- historic-missouri-bill-shows- momentum-for-ewa-registration/ ; State of Montana, Attorney General Opinion by Austin Knudsen, Attorney General, December 22, 2023, Montana Administrative Register, Vol. No. 59, Op. No. 2, available at https://dojmt.gov/wp- content/uploads/2024/11/Vol.- 59-No.-2-arm.pdf; Payactiv, Inc., Payactiv is now a Licensed Earned Wage Access Provider in Nevada, April 21, 2025, https://www.payactiv. com/blog/payactiv-is-now-a- licensed-earned-wage-access- provider-in-nevada/; Payactiv, Inc., South Carolina Governor Signs Earned Wage Access Bill into Law, May 23, 2024, https://www.payactiv. com/blog/south-carolina- governor-signs-earned-wage- access-bill-into-law/; Payactiv, Inc., Payactiv is Now Officially Registered as an Earned Wage Access Provider in Utah, June 26, 2025, https://www.payactiv. com/blog/payactiv-is-now- officially-registered-as-an- earned-wage-access-provider- in-utah/ ; Payactiv, Inc., Payactiv Licensed in Wisconsin Following EWA Legislation Enactment, April 8, 2026, https://www.payactiv.com/blog/payactiv-licensed-in-wisconsin-following-ewa-legislation-enactment/ - “The root of factoring is the transfer of risk.” Endico v. CIT (2d Cir. 1995). See also K9 Bytes, Inc. v. Arch Capital Funding, LLC, 56 Misc. 3d 807, 816 (Sup. Ct. Westchester Cnty. 2017) (“In determining whether a transaction is a loan or not, the court must examine whether or not defendant is absolutely entitled to repayment under all circumstances.”); Merch. Cash & Capital, LLC v. Yehowa Med. Servs., Inc., 2016 NY Slip Op 31590, at *5 (Sup. Ct. Nassau Cnty. July 29, 2016); Prof’l Merchant Advance Capital, LLC v Your Trading Room, LLC, 2012 NY Slip Op 33785[U], *6 (Sup Ct., Suffolk Cnty. N.Y. Nov. 28, 2012) (“[plaintiff] failed to establish that the subject agreement to purchase credit card receivables was a loan and not an agreement to purchase future receivables for a lump sum discounted purchase price payable in advance by the plaintiff in exchange for a contingent return”).

- State of Arizona, Attorney General Opinion by Mark Brnovich, Attorney General, December 16, 2022, No. I22-005 (R22-011), Re: Earned Wage Access Products, available at https://www.azag.gov/opinions/i22-005-r22-011

- State of Montana, Attorney General Opinion by Austin Knudsen, Attorney General, December 22, 2023, Montana Administrative Register, Vol. No. 59, Op. No. 2, available at https://dojmt.gov/wp-content/uploads/2024/11/Vol.-59-No.-2-arm.pdf

- In California, payroll deductions are permitted “when a deduction is expressly authorized in writing by the employee to cover insurance premiums, hospital or medical dues, or other deductions not amounting to a rebate or deduction from the standard wage arrived at by collective bargaining or pursuant to wage agreement or statute [. . .].” Cal. Lab. Code § 224 (emph. added). See also Lemus v. Denny’s, Inc., No. 11CV2131-CAB WVG, 2013 WL 10730259, at *1 (S.D. Cal. Mar. 21, 2013), aff’d in part, 617 F. App’x 701 (9th Cir. 2015) (“[A]s long as the deduction is ‘expressly authorized in writing’ and does not amount to ‘a rebate or deduction from the standard wage (a standard wage arrived at by collective bargaining or under wage agreement or statute),’ then the deduction is authorized under section 224.”).

- Mo. Code Regs. tit. 8, § 30- 4.050.

- M G.L. c. 29, § 150; M.G.L. c. 149, § 148.

- While the FLSA does not govern EWA, the most analogous rule is set forth in Department of Labor’s Field Operations Handbook, which expressly permits deductions for wage advances. See ch. 30c10.

- Courts have noted a “legislative intent to protect wage earners and salaried workers against the possibility that, either from improvidence or under the stress of immediate necessity, they may go too far in sacrificing the future to the needs or desires of the present and leave themselves and their families without future means of support.” Lande v. Jurisich, 59 Cal. App. 2d 613, 615 (2d Dist. Ct. of Appeal 1943) (emphasis added).

- Federal Reserve Board, Staff Guidelines on the Credit Practices Rule; see also In re Johnson, 554 B.R. 448, 455 (Bankr. S.D. Ohio 2016), aff’d, No. 16-8035, 2017 WL 2399453 (B.A.P. 6th Cir. June 2, 2017) (finding that the purpose of California Labor Code Section 300 is to protect wage earners from assigning their future wages). The Federal Trade Commission’s Credit Practices Rule also declares “unfair” and therefore “unlawful” any loan contract containing an irrevocable wage assignment—defined as a provision in which “the debtor assigns future wages to the creditor in the event of default.” 16 C.F.R. § 444.2(a)(3) (emph. added). Notably, an exception to the FTC’s prohibition suggests a close analogy to Payactiv’s EWA program, where payment is triggered not by default but instead is part of “a payroll deduction plan or preauthorized payment plan, commencing at the time of the transaction, in which the consumer authorizes a series of wage deductions as a method of making each payment.” 16 C.F.R. § 444.2(a)(3)(ii).

- See, e.g., CFPB v. UniRush LLC, No. 2017-CFPB-0010 (Feb. 17, 2017) (prepaid provider paid $13 million following processing error that resulted in delayed payment of wages).

- Todd Baker and Snigdha Kumar, The Power of the Salary Link: Assessing the Benefits of Employer-Sponsored FinTech Liquidity and Credit Solutions for Low-Wage Working Americans and their Employers, M-RCBG Associate Working Paper Series No. 88 (May 2018), available at https://www.hks.harvard.edu/sites/default/files/centers/mrcbg/working.papers/88_final.pdf (last accessed Nov. 13, 2020). See also Center for Social Development at Washington University in St. Louis, Workplace Financial Wellness Services: A Primer for Employers, (2017), at 10 available at https://csd.wustl.edu/17-33/ (last accessed Nov. 13, 2020) (noting that Payactiv’s EWA helps employees “eliminate[] costly short-term loans” and “moderate income volatility”).

© 2026 Payactiv, Inc. All Rights Reserved

24 hour support: 1 (877) 937-6966 | [email protected]

* The Payactiv Visa Prepaid Card and the Payactiv Visa Payroll Card are issued by Central Bank of Kansas City, Member FDIC, pursuant to a license from Visa U.S.A. Inc. Certain fees, terms, and conditions are associated with the approval, maintenance, and use of the Card. You should consult your Cardholder Agreement and the Fee Schedule at payactiv.com/card411. If you have questions regarding the Card or such fees, terms, and conditions, you can contact us toll-free at 1-877-747-5862, 24 hours a day, 7 days a week.

** Central Bank of Kansas City does not administer, nor is liable for earned wage access.

Payactiv, Inc.

NMLS ID: 2591928

Payactiv holds earned wage access services (EWA) license number 2591928EWA with the Wisconsin Department of Financial Institutions.

Payactiv holds small loan license number SLC-2591928 with the Connecticut Department of Banking.

Payactiv holds earned wage access services (EWA) license number EWA00009 with the Nevada Financial Institution Division.

Apple and the Apple logo are trademarks of Apple Inc., registered in the U.S. and other countries. App Store is a service mark of Apple Inc., registered in the U.S. and other countries.

Google Play and the Google Play logo are trademarks of Google LLC.

Galaxy Store and the Galaxy Store logo are registered trademarks of Samsung Electronics Co., Ltd.