How FinTech Creates Fin-Tax on the Working Class

For 60 million families living paycheck to paycheck, PayDay loans are just the tip of a titanic financial iceberg

I am thrilled to be joining Safwan Shah and his team of PayActivists (as a director).

PayActiv is delivering a much-needed, much-deserved financial product, to help the families who are living paycheck to paycheck.

We know we can save millions of families from the estimated $1,200 annual Fin-Tax (more on that below) and help them get that money back for their families, use it to buy within their communities, and enjoy a reduction in financial stress in the bargain.

- What is a Fin-Tax? It is the unintended consequence of FinTech

- Employees are lenders, to their own employers

- It is easier to be poor, when you have money

- Empathy: walk a mile in their shoes

- Nibbled to death by sharks. Let’s take a tour of financial life as ‘prey’

- Are you starting to feel trapped?

- PayActiv Stories: Why we are in the business

- A final word, on velocity of money

- Your call to action, and a question

What is a Fin-Tax? It is the unintended consequence of FinTech

The FinTech (Financial Technology) world is powered by cleverly devised software that hunts ruthlessly for return (like, say, the Terminator — the software never gives up). It is not a singular effort, but a combined one, through PayDay Lenders (the most reviled, but a smaller player) to Credit Card companies, Banks, Title Lenders, Debit Card issuers, Gift Card issuers, Cellphone Carriers, Auto Lenders, and even Landlords.

That combined FinTech effort creates what we call a Fin-Tax on families living paycheck to paycheck. An average of $1,200 per year, per family, that goes out of circulation and into the financial system. A very heavy tax on a net income that can be as low as $15,000.

There are over 60 million working families who do not have $400 in savings, to meet the emergencies in life. They are underbanked, and overcharged.

Checking fees. Late fees. Overdraft fees. Payday loan fees. Title loan fees. Phone re-start fees. It goes on and on, it is harsh, it takes a big chunk out of take-home pay, and parks the money in the financial system, out of circulation.

FinTech helps lenders ‘risk adjust’ their rates, but in doing so, pools are created that drive rates that make finance charges a substantial piece of the worker’s take home pay.

And yet, employees are lenders, to their own employers

These Fin-Taxes are levied in real time, relentlessly. And yet, the working family has an asset, their earned but unpaid wages, locked into the paycheck cycle.

It is one of the unintended consequences of the payroll system that has the working poor acting as lenders to their employers, even while they are hit left, right, and center with Fin-Tax fees, because their money is tied up in a loan to the employer.

PayActiv is a platform for employers to enable employees to access their earned, but unpaid, wages, which can be used to pay bills, avoid late fees, avoid overdrafts, avoid Payday Lenders, buy smarter.

It is easier to be poor, when you have money

You don’t lose $1,200 of your net income to Fin-Tax fees.

You can afford preventive maintenance on your car, and avoid costly breakdowns.

You can shop for bargains, and stock up on deals. (Most coupons are actually redeemed by the very well-off.)

You don’t have to pay $10–25 dollars a month for a checking account.

You can keep your credit card balance low, or even pay it off, and avoid paying interest, AND get 1–2% credit in cash rebates or points.

You don’t have to worry about getting your phone, or utilities, or Internet turned off (and pay re-start penalties).

You pay a rational interest rate on a manufacturer-subsidized car lease or car purchase.

You can live cheaply, and live without worry, if you have money. Try it without money, and you begin to feel you are trapped, and for good reason. You are.

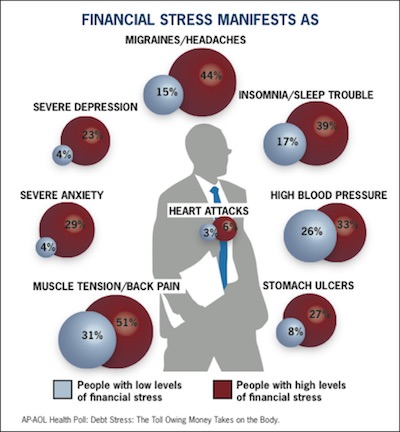

Empathy: walk a mile in their shoes

A direct byproduct of financial stress is mental stress, which is detrimental to the efforts of the employees, and the companies where those employees work.

Think of the last time you had what you saw as an unfair and onerous event, like an expensive traffic fine, or a big DMV penalty, or a nasty surprise at your home that became expensive. You remember how unhappy that made you, how it stressed your day or week, how you possibly posted on social media how upset you were at the injustice of it all?

Well, then, imagine getting hit with (proportionally) similar financial nastiness two or three times a month, and you can start to feel the pain that the Fin-Tax creates for families who are working but surviving paycheck to paycheck.

It is no wonder that at companies using PayActiv, the employees who are active on the platform have 20–30% lower turnover, which is a massive savings in costs, especially when you consider PayActiv is free to the employer. The only fee is paid by the employee when they access their money.

But wait, it gets better: the impact on the employee base is so positive, many of our employers are paying all or part of the fee, because the measurable financial wellness delivered is so valuable.

Nibbled to death by sharks. Let’s take a tour of financial life as ‘prey’

(Most of this data is via the CFSI Underbanked Study, available here.)

Overdraft Fees

(CFSI*)Payday Lenders are the visible ‘sign’ of the underbanked, but their fees are dwarfed by the Overdraft fees of banking institutions, and the vast majority of those fees come from the working poor. If you overdraw the account, a returned check fee is $25–40! And, if you subscribe to overdraft protection, then going even $1 over triggers a $27 (on average) fee. And, if you have borrowed from other sources, and they can ‘ding’ your account, when they do, and the funds aren’t there, more $27 (on average) charges. So even if you get into the ‘mainstream’ banking system, your errors, duly noted by FinTech software, will add up to a sum of fees that is 50% LARGER than the revenues of the entire U.S. music industry.

Bank Account and Money Fees

(CFSI*)When you have a lot of money, banks are your friend. When you have a little, not so much. If you can’t maintain a minimum balance (remember, 40% of families don’t have $400) then you pay $10-25 a month to run a checking account. And, if you take out some cash, another $2–4 fee. And if you are with the big banks, maybe another $5 per month to use a debit card. Want to send a $100 money order? That’s $1.25 at the USPS, can be $5–6 at a credit union or bank (and they say the government is inefficient!). Want to cash a check but don’t have a bank account — at least 20% of Americans? You pay at most banks if you go directly to the issuing bank to cash the check, often $5–6. You can go to a 7–11 and pay a .99% fee, one of the most reasonable. Check Cashing and PayDay Lending stores will charge up to 10% of the value. Trying to save money? Remember most underbanked don’t have $400 in savings. Banks such as Bank Of America charge $5/month for a savings account with a balance less than $300.

Subprime and Title Loan Fees

(Various Banks for the Unbanked, including Collateral Lenders, Installment Loans, Subprime Credit Cards): (CFSI*)

- Title Loans and Pawn Shops. The Pawn business is almost as old as banking itself; the three-ball symbol is descended from the Medici’s in Lombard. You need money and have some property with some value. Many storefront lenders provide both services, as well as Payday loans.

- Title Loans. About 2 million people use Title Loans each year, using their automobile as collateral. The lender ‘holds’ the title document until the loan is repaid. Per BankRate: About 7,730 car title lenders operate in 21 states, charging borrowers $3.6 billion in interest on $1.6 billion in loanseach year. A typical borrower receives cash equal to 26 percent of a car’s value and pays an annual percentage rate of 300 percent.

- The Pawn Shop is a ‘title loan,’ but without a title document, because the Pawn Shop retains possession of the property itself. Collateral lenders make most of their money from interest and fees; in the United States, per Wikipedia, 11,000 pawnbrokers earned $14.5 Billion in revenue from 30 million customers. They will offer you considerably less ‘loan’ against your collateral than a sale on eBay (you have to have margin, of course) but you have two advantages — you can still repay and get your goods back, and it is a non-recourse loan. 80% of pawned goods are reclaimed, 20% are forfeited. For this you pay a combination of regulated interest, from 5% to 25% PER MONTH, plus a service charge that can be as high as 20% per month. So, that $375 loan could cost you $75 a month in interest and fees.

- Subprime Credit Cards. If you are underbanked and need a credit card, you can get one, but it will cost you an obscene amount of your money — almost as much money is generated in fees for SubPrime cards as are generated by PayDay Loans. For example, a typical offer for a $300 Subprime credit card includes “Annual Fee of $49, Account Processing Fee of $99, Program Participation Fee of $89 and monthly Account Maintenance Fee of $10.” You are then notified: “ Your available credit after these charges will be $53 at Card issuance (for a $300 line).”(Bankrate). You can cry now.

- Installment Loans. This market alone is almost as big as Payday Loans. You can borrow more, say, up to $2,600, and pay back over a longer period of time. Here is the disclosure info (not readily available outside the small print) for a typical Installment Loan: Advance Amount: :$2,600. Finance Charge: $9,863.87. Total of Payments: $12,463.87. Loan Origination Fee:$75. Doesn’t the Bible have something to say on this?

SubPrime and Buy Here Pay Here Auto Loans

- SubPrime Auto Loans:

Most people need a car to get to work, and to manage a family. In many areas, working class employees need to live some distance from the affluent areas where they work, and these are, in most instances, not served by public transportation. So, cars a necessity for work and a paycheck.

Now, consider a 60-month loan amount of $16,333. Per Bankrate, a Nonprime borrower would pay 9.29 percent interest, $341 per month for 60 months, a total of $20,460. A Subprime borrower for that $16,333 loan would pay $394 for 60 months, or a total of $23,640. A Deep subprime borrower for that $16,333 loan would pay $423 per month for 60 months, $25,380 total. A cash buyer would likely get a discount, and pay $16,000. A Prime borrower would pay a total of around $18,000.

Given the state of the economy and the challenges facing working families, it should be no surprise that the percentage of auto loans to buyers with the poorest credit ratings is growing faster than the rest of the auto finance market (about a third of all new car purchases).

The difference between prime lending rates and deep subprime, on that $16,333 car loan, comes to $123/month, or $1,476 per year. Of course, you can buy a Honda Odyssey family mini van with 150,000 miles for half that or less, but there will be repair bills at some point.

It may not be completely fair to count the entire $24 Billion annually of Subprime fees as part of the ‘Fin-Tax,’ but about $16bn of it is the higher interest charged to credit buyers who are poor.

- Buy Here Pay Here Auto Loans (on some lots, known as Dealer Financing.)

A form of Subprime Lending, this category is financing by auto dealers who loan directly to the buyer. The buyer is typically unable to borrow anywhere else, and the seller can charge double-digit interest, often making more on the financing than the vehicle itself. As with Subprime Auto Loans, the $18.3 billion of Buy Here Pay Here is about $12 billion higher than buyers with good credit will pay.

Late fees

(CFSI does not calculate these, so this our conservative calculation.) Late with the rent, or a car payment, or the phone payment, or the internet payment? There is a fee (a Fin-Tax) for that, and it adds up. Late payment fees, reconnection fees, and more, are a way of extracting more LTV from customers. Cell lines are vital, and, many working people can’t afford a home connection AND a cell line, so rely on WiFi at work and at home, and that means the Internet connection is just as vital as a cell connection.

And, Payday Loans and Anticipation Fees

(CFSI*) $8 Billion in fees; $40 Billion loaned. You need $375. There are 21,000 retail locations for payday loans (literally, loans until your next payday) and numerous websites. You now owe $415 from your next paycheck. If you can’t pay, you can ‘roll it over;’ the typical borrower takes out eight such loans a year and pays a total of $520 in interest (for the re-use of $375). Lenders, in turn, make 80% of their money on ‘rollover’ loan fees and interest. If the lender has the right to ding your bank account, they will, often for small amounts so that they can get as much cash as possible, stopping when there are no funds, and then you are hit with an average $27 overdraft fee, and that can be many times a year. Those lenders retain the right to collect or sue; they can (and do) sell the loan at a discount to collections agencies who do nothing but make your life miserable, going for the full amount. Retail payday lending is very inefficient; a storefront might serve several hundred customers per year, and must pay rent, salaries, and lost capital over that small number. Online lenders aren’t much better.

Anticipation Fees are a form of Payday Loans, but the ‘collateral’ is the tax refund. Terms can be onerous, the lender retains the right to the tax refund as collateral, and interest rates are many times higher than a credit card, and these are augmented by any number of Application, Service, Transmission, Document Processing, and other fees.

Are you starting to feel trapped?

Millions of people are. How do you climb out when your pay barely covers the bills, and every mis-step reduces your pay with penalties and fees, and when you then wind up paying $27,000 for a $16,000 car, pay hundreds to maintain a bank account, pay hundreds to have a credit card?

Well, we have a start.

PayActiv Stories: Why we are in the business

Here are the issues:

“I missed work because I couldn’t pay the babysitter. I don’t get my paycheck for 3 more days.”

“I pay $50 late fee on rent because if I pay it on time then I can’t go through till my next paycheck.”

“My car broke down and I didn’t have enough to get it fixed.”

“I was short only a few bucks but got hit by a $25 overdraft fee.”

“Last month I couldn’t pay my phone bill, ended up with late fee plus a $45 restoration fee.”

And here are the stories:

PayActiv can’t solve the entire Fin-Tax burden on the working poor, but we can alleviate much of it when employers provide our service to their employees. Often we turn a vicious spiral into debt traps into a virtual spiral to solvency.

“I have 3 kids and my husband and I both work. We have no savings and my dream is to save up to be a homeowner one day. I have paid overdrafts at least 4 times over this past year. And I have paid $25 late fee on rent 6 times the last one year. PayActiv has helped me avoid late and overdraft fees. “

“I don’t like being late but sometimes I just didn’t have enough to cover. I used to pay $50 for late fees on my rent. With PayActiv now I just access my own cash.”

“I had to borrow from a payday lender when my car broke down. He took $45 for a $300 loan and gave me $255. I never wanna go back. I can just access PayActiv if I need some money like that.”

“I have a bank account but I used to pay overdraft fees every time my rent was due. Now I use (PayActiv) for rent and groceries. Everything else can wait until payday.”

“It felt great to start paying off payday loans and now at this point I am out of them. PayActiv really really helped.”

“I like to know that I have the option to withdraw money when I need it. It’s my back up. It makes me feel secure.”

“I use PayActiv to pay my bills on time. I don’t like getting charged late fees. I don’t got a lot of money to be giving away like that.”

A final word, on velocity of money

The PayActiv ‘big dream’ is to serve 10 million of these employees, helping them avoid $6–12 Billion in Fin-Tax fees. (We estimate that each $5 fee to access unpaid wages enables the employee to avoid a minimum of $30 in overdraft, borrowing, late fees, and other charges, often more, not to mention other stresses.)

Doing so is a boon to the employers who use the platform, lowering employee financial stress and turnover.

It puts money back in the pockets of working people for things like clothes and school and food. It circulates through their communities, instead of being lodged up in a finance giant’s balance sheet. And, in doing so, PayActiv is becoming a valuable company, by delivering this much-needed value.

Your call to action, and a question

If you manage or supervise or work at a company where there are people making less than $50,000 a year, please have a look at PayActiv. You will make employee lives better, that is a good thing. And you’ll improve your company ‘expenses without invoices,’ such as employee turnover. Ping me and I’ll send you a Stress Ball, and a Case Study.

And my question: It appears to me that the trend to income inequality (money flowing to the top of the pyramid to the point where the top 1% in America control 40% of the wealth and 90% of the income gains) is reflected, or perhaps, magnified, by an inverse fee structure — the bottom 50% pay the fees, penalties, higher interest, and more, that make up a bulk of profits for many financial institutions. What do you think is the solution?

(Also read: Five Reasons to Help Your Employees Avoid Fin-Tax)

Get Payactiv for your business

Learn how thousands of companies have improved their retention, recruitment, and engagement by offering Payactiv.

Request a Demo

Related Articles

For many people, their first big purchase is their first car You need a vehicle...

Over half of North American employees are more stressed about their finances...

In today’s uncertain economic climate, financial struggles affect...