Understanding Your Credit Score and How to Improve It

What is a credit score and why does it matter? Learn more in this guide to credit health.

Your credit score is one of the most important numbers in your financial life. It’s a three-digit number representing how reliable you’ve been at repaying borrowed money in the past. Lenders, and even some landlords and employers, use your credit history to decide whether to offer you loans, rental agreements, or jobs.

Credit scores typically range from 300 to 850. A higher score means you’re a lower risk to lenders, which can help you qualify for better loan terms, lower interest rates, and more financial opportunities. A lower score, on the other hand, can make it harder to get approved for credit or result in higher interest rates, costing you more in the long run.

How Credit Scores Are Calculated

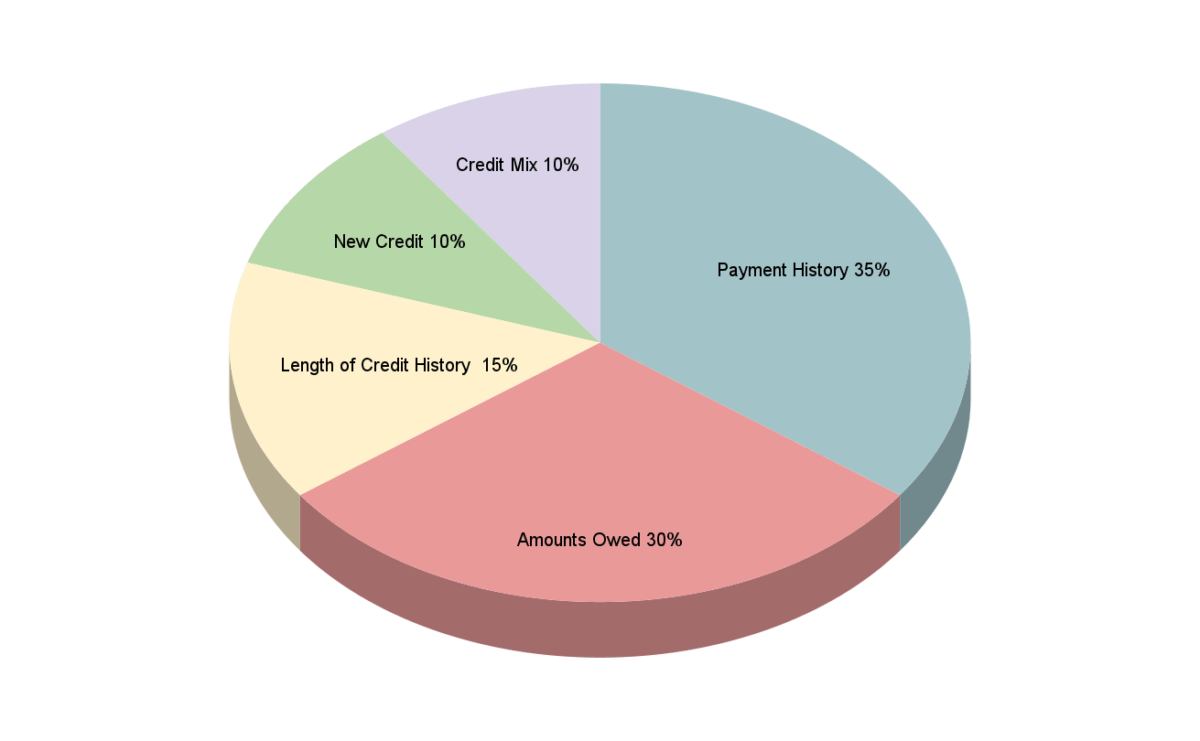

Credit scores are calculated using information from your credit report, which details your borrowing and repayment history. The main factors influencing your score include:

- Payment History (35%) – On-time payments are the biggest factor in your credit score. Late payments, defaults, and collections can hurt your score significantly. The most important part of credit building is making every payment on time.

- Amounts Owed (30%) – The total amount of debt you have compared to your total available credit (credit utilization ratio) is the second biggest factor in your credit score. Keeping credit card balances low can help improve your score. The fastest way to improve your score, in many cases, is to pay off your credit card balances.

- Length of Credit History (15%) – The longer you’ve had credit accounts open, the better. Having older accounts in good standing shows responsible credit use over time. Opening new cards lowers your average age of credit, while keeping cards open for a decade or more can help your score, as long as you keep balances low and always pay on time.

- New Credit (10%) – Opening too many new accounts in a short period can temporarily lower your score because it signals potential financial distress. If you keep the balances low and always make on-time payments, the accounts should eventually help your credit.

- Credit Mix (10%) – A diverse mix of credit types, such as credit cards, auto loans, and mortgages, can be beneficial, as it shows you can handle different types of credit responsibly. However, it’s generally not a good idea to open new accounts just to improve your credit mix.

How to Check Your Credit Score and Report

Checking your credit score and report regularly is a good financial habit. You can get a free credit report once a year from each of the three major credit bureaus, Experian, Equifax, and TransUnion, through AnnualCreditReport.com. Many banks and credit card companies also offer free credit score and credit report access to their customers.

When reviewing your credit report, look for:

- Errors or inaccuracies – Check for incorrect balances, accounts that don’t belong to you, or late payments that you actually made on time.

- Signs of fraud – If you see accounts you don’t recognize, you may be a victim of identity theft. These require immediate attention to prevent the problem from getting worse.

- Missed payments – Make a plan to catch up and avoid future missed payments. Late and missed payments typically stay on your credit report for seven years.

How to Improve Your Credit Score

If your credit score is lower than you’d like, there are steps you can take to improve it over time.

1. Pay Your Bills on Time

Since payment history is the biggest portion of your credit score, always aim to pay at least the minimum amount for all bills by their due dates. Setting up automatic payments or reminders can help you stay on track. If you’re a little short before payday, look into getting part of your paycheck early with Payactiv.

2. Reduce Your Credit Card Balances

Your credit utilization ratio (how much of your available credit you’re using) plays a significant role in your score. While many experts suggest keeping your credit usage below 20% to 30% of your available balances, the best utilization rate for your credit score is 0%. Contrary to a popular myth, you don’t need to carry a balance to build credit.

3. Avoid Applying for Too Many New Accounts

Each time you apply for a new credit account, a hard inquiry is recorded on your credit report, which can slightly lower your score. Apply for new credit only when necessary. Hard inquiries generally lower your score by just a few points and go away after two years, so they shouldn’t be a reason to avoid new accounts if you really need them.

4. Keep Old Accounts Open

Closing older credit accounts can shorten your credit history length, which may negatively impact your score. If your accounts are in good standing, try to keep your oldest accounts open to maintain a longer credit history.

5. Dispute Credit Report Errors

Mistakes on your credit report can hurt your score, and they’re much more common than many people realize. If you find an error, dispute it with the credit bureau that issued the report. They are required to investigate and correct any inaccuracies.

How Long Does It Take to Improve a Credit Score?

Improving your credit score takes time and consistent effort. Small changes, like making on-time payments and reducing debt, can start to show results in a few months. However, more significant improvements, such as recovering from missed payments, can take many months to several years.

Because excellent credit can be ruined quickly and takes years to rebuild, it’s best to get into good financial habits and stick with them. Your financial health will be much better for it.

Take Control of Your Credit Today

Your credit score isn’t set in stone. You’re in control over your credit, and you can work to improve your credit score over time with good financial habits. By understanding how credit works, checking your credit report regularly, and consistently improving credit-related habits, you can build a strong credit foundation that opens doors to better financial opportunities.

Start today by checking your credit report and making a plan to improve your score. Small steps today can lead to enormous financial benefits in the future.

All content provided on Payactiv.com/financial-learning/ is for informational purposes only. Payactiv makes no representations as to the accuracy or completeness of any information on this site or found by following any link from this site. Payactiv will not be liable for any errors or omissions in this information nor for the availability of this information. Payactiv will not be liable for any losses, injuries, or damages from the display or use of this information.

Get Payactiv for your business

Learn how thousands of companies have improved their retention, recruitment, and engagement by offering Payactiv.

Request a Demo