April 15, 2026

|

Blog

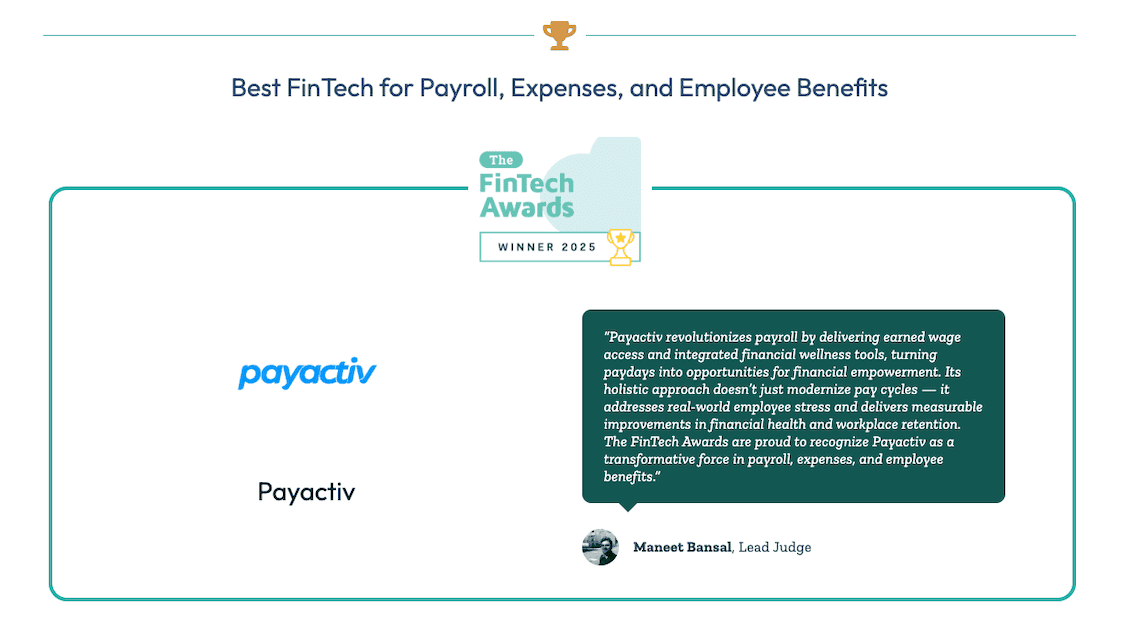

We are honored to share that Payactiv has received a top award in the Best FinTech for Payroll, Expenses, and Employee Benefits category at the 2025 FinTech Awards, presented by The Cloud Awards This recognition from The Cloud Awards confirms […]