Payday Pulse: Where Americans Are Most Burdened By Household Debt

Household debt is not just a number on a statement. For many families, it becomes the tool they use to keep life moving when costs hit before cash does.

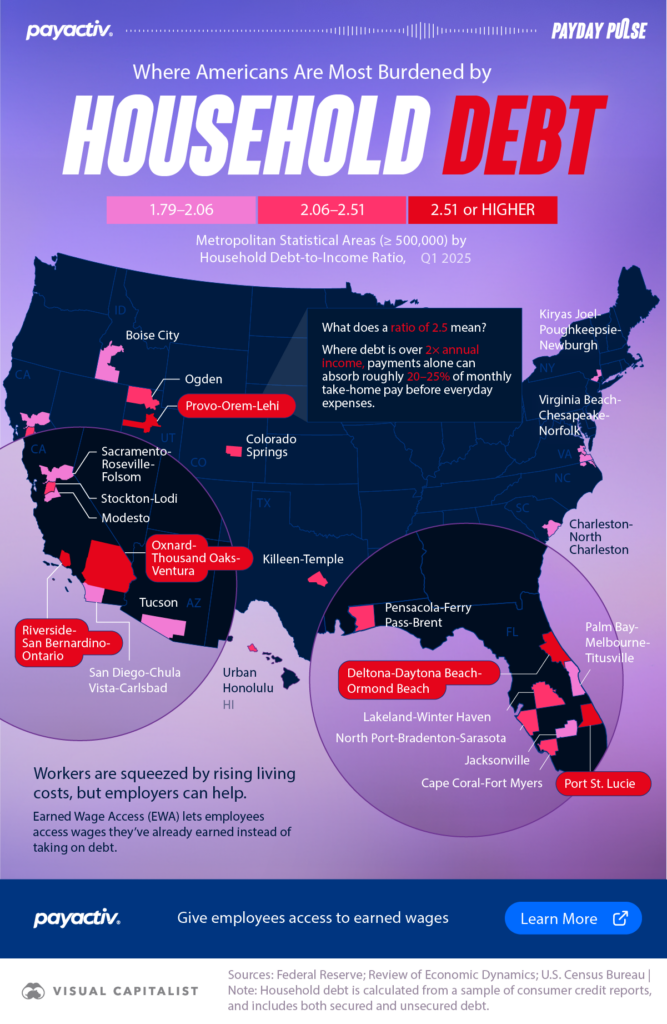

Payactiv partnered with Visual Capitalist to map where household debt is creating the greatest pressure. In Payday Pulse: Where Americans Are Most Burdened By Household Debt, we take a data-driven look at the 25 U.S. metro areas with the highest household debt-to-income ratios and what those ratios can reveal about financial pressure in everyday life.

The Gap Debt Is Asked To Fill

Most people do not take on debt because they want to. They take it on because life is expensive and the timing rarely lines up. Rent and mortgages are due on a fixed date. Groceries run out when they run out. A car repair shows up at what seems like the least affordable and most inconvenient moment.

Paychecks, on the other hand, arrive on a schedule that is not designed around those moments.

When budgets are tight, even a short gap can create a tough choice. Do you pay late and take the fee, or pay now and deal with potentially snowballing interest? Over time, those small decisions can become a pattern, and that pattern can turn debt into a constant monthly bill that begins eating up a limited income before you even think about anything else.

What High Debt-To-Income Ratios Really Mean

In places where debt-to-income ratios are high, the pressure rarely comes from just one type of loan. Mortgages, auto loans, student loans, and credit cards can stack together, and the mix can vary by metro. The common thread is simple: the total balance is high relative to wages, leaving less room for unexpected costs.

A debt-to-income ratio above 2.5 indicates that a household owes more than 2.5 years of wages in total debt. That does not automatically mean payments are impossible, but it often means the budget has less flexibility, and the household is more financially fragile and likely to end up in a situation where debt payments get out of control.

When so much of the month’s income is already spoken for, a single timing issue can lead to a limited set of difficult, expensive choices. But when the worker has access to Earned Wage Access (EWA)1 through their employer, they can get access to a portion of their wages, often instantly or near-instantly, with no interest charges.

Why The Pressure Shows Up In Specific Places

High ratios often appear in regions where housing costs have climbed faster than wages, where populations are growing quickly, or where commuting and transportation costs are hard to avoid. It is not just a coastal story. It is a national story that looks different depending on the local cost of living, the types of jobs available, and how far households need to stretch to stay in place.

That is why you can see the same states appear repeatedly while still finding high-debt pressure nationwide. The details change by metro, but the experience is familiar. Costs rise, pay schedules are static, and credit becomes the bridge when a cash crunch or financial emergency appears.

Pay Timing Is A Powerful Lever

Debt can support long-term goals, and many families use it responsibly. However, problems arise when debt becomes a major cost when managing short-term cash flow gaps. When bills come due before payday, households can end up paying extra just to access money sooner, even though they have already earned it.

If used responsibly, Earned Wage Access can completely eliminate the need to pay interest or make loan repayments in the future. EWA lets employees access a portion of wages they have already earned before the end of the current pay period, so they can ideally cover essentials without borrowing against future pay.

It works alongside existing payroll systems and can help align pay and bill timing, especially for workers already carrying heavy debt.

Explore Payday Pulse

Explore Payday Pulse: Where Americans Are Most Burdened By Household Debt to see where the highest debt-to-income ratios are concentrated and why pay timing is part of the pressure many households feel between paychecks.

1Earned Wage Access requires employer participation. Employees can only access a portion of the wages they have earned to date.

All content provided on Payactiv.com/financial-learning/ is for informational purposes only. Payactiv makes no representations as to the accuracy or completeness of any information on this site or found by following any link from this site. Payactiv will not be liable for any errors or omissions in this information nor for the availability of this information. Payactiv will not be liable for any losses, injuries, or damages from the display or use of this information.

Get Payactiv for your business

Learn how thousands of companies have improved their retention, recruitment, and engagement by offering Payactiv.

Request a Demo