Payday Pulse: America’s Growing Mountain Of Debt

Debt in America is often framed as one big, abstract number. But for many working households, debt shows up in countless daily decisions, from what to pick at the grocery store to juggling utility bill due dates. While some people use debt as a tool to reach important goals, like homeownership, it can be financially crippling for others. And when borrowing for short-term needs, debt can become much more expensive.

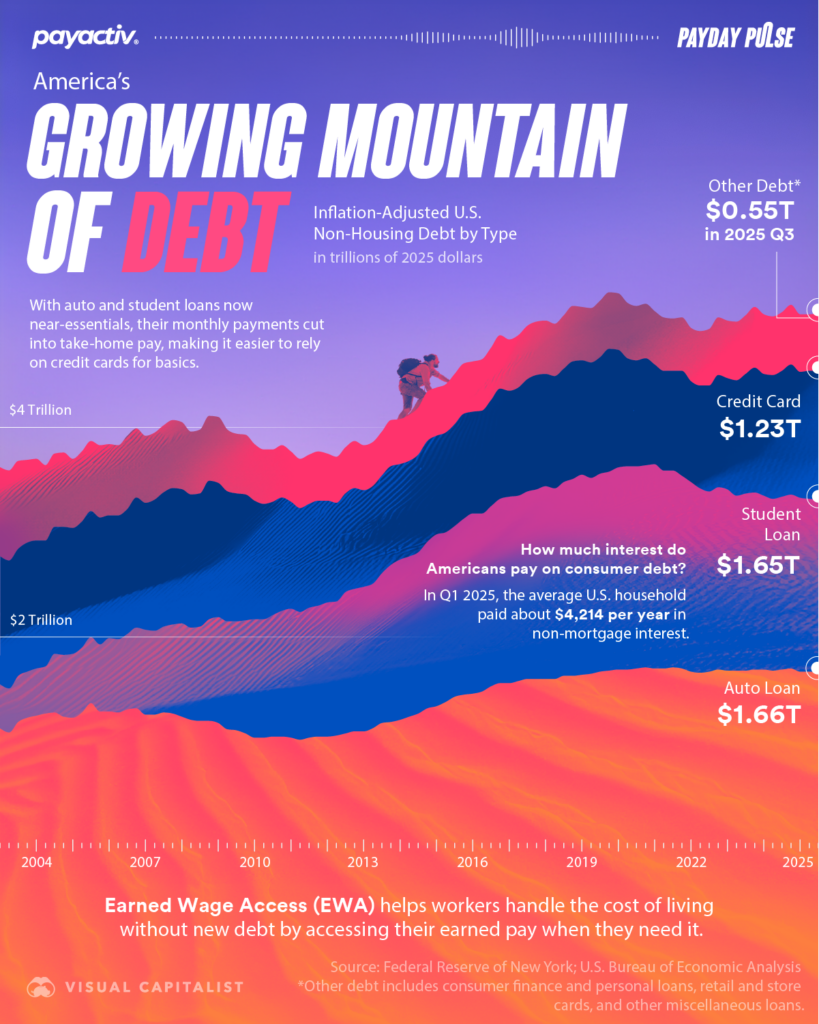

Payactiv partnered with Visual Capitalist to explore America’s Growing Mountain of Debt. When money is earned on one schedule and bills arrive on another, even strong budgeting habits can fail. Over time, that timing mismatch can turn borrowing from an occasional fallback into a repeating monthly pattern. Follow along for this breakdown of America’s latest debt trends.

From Enabling Large Purchases to Bridging the Gap

For decades, debt was mainly tied to major financial milestones: a new car, a college degree, a home purchase. Those still matter, but the everyday role of debt has expanded. Higher costs for nearly everything we buy have made the month less forgiving, leading more households to use credit to stay flexible when they can’t cover the bills.

That pressure shows up in familiar moments:

- A rent or utility bill lands days before payday

- Groceries and gas spike in the same week as a child expense

- A repair hits at the least convenient time, with no buffer available

When those moments keep repeating, interest and fees begin acting like their own recurring bill.

A Cycle Of Setbacks And Rebuilding

The long-term trend in non-housing debt is not a straight line, but it does have a pattern. After major economic shocks, balances can fall as households default, pay down debt, and pull back spending. Then, as the economy stabilizes, balances rebuild and continue climbing.

The challenge is what happens when borrowing becomes the default response to tight timing. In higher-rate environments, the same balance costs more to carry. That can tighten household cash flow even further, especially when larger shares of take-home pay are committed to fixed monthly payments before the month really begins.

Auto And Student Loans Stand Out in Monthly Budgets

Two categories stand out because they often fund things people treat as near-essentials.

Auto loans are not just about a vehicle. For many workers, a car is what makes employment possible, especially in regions where commutes are long or public transit is limited. Student loans are not just about education. For many households, they represent the price of credentials needed to reach higher wages.

As of the latest available data, auto loans and student loans sit near the top of America’s non-housing debt categories, alongside credit card balances. The key point is not just the totals. It is how these obligations shape the monthly budget. When large payments are fixed, there is less room for volatility, and more of life ends up financed.

Why Credit Cards Become The Default Bridge

Credit cards are often the fastest way to manage a short-term shortfall. They can cover essentials when timing is off and keep a household afloat during a tight week.

The downside is what happens when a “bridge” becomes routine. If balances carry month to month, interest starts compounding, minimum payments become another obligation, and building a buffer gets harder. That is how timing gaps turn into longer-term debt pressure without any dramatic change in spending behavior.

Pay Timing Is A Practical Lever Employers Can Offer

The most frustrating part of cash flow stress is that the work has already been done. The wages are earned, but access is delayed by a payroll schedule that was built for administration, not bill timing.

Earned Wage Access (EWA)1 can help reduce reliance on interest-bearing options by letting employees access a portion of wages they have already earned during the pay period through an employer-connected payroll flow. It does not replace payroll. It adds flexibility around it, so workers have more options when bills come due before payday.

Where EWA makes a measurable difference is in the avoidable costs layer, helping employees prevent expenses such as:

- Interest charges that come from short gaps, not long-term plans

- Late fees triggered by timing, not inability to pay

- Repeated reliance on credit for essentials between paychecks

Explore America’s Growing Mountain of Debt

Explore Payday Pulse: America’s Growing Mountain Of Debt to see how non-housing debt has shifted over time and why pay timing remains a major factor in financial pressure between paychecks.1Earned Wage Access requires employer participation. Employees can only access a portion of the wages they have earned to date.

Get Payactiv for your business

Learn how thousands of companies have improved their retention, recruitment, and engagement by offering Payactiv.

Request a Demo