Bridging the Gap to Financial Wellness

Podcast: Play in new window | Download

The employer-employee relationship is at the heart of every company’s success. Yet you’re probably thinking about it all wrong.

We’re pleased to present this pre-recorded session of Payactiv CEO Safwan Shah providing a wide-ranging exploration into the meaning of employee financial wellness. It’s not what you think.

From the surprising connection between happiness and money, to the truth about adult financial literacy (or lack of it), this Ted-style talk will cause you to re-evaluate your best practices for supporting your employees.

This presentation was first delivered at the HR.com Financial Wellness Programs Virtual Event on March 3, 2021.

Read the highlights

The first point that we will cover in detail is why despite the growth and financial wellness offerings are workers still unwell. The word financial wellness has been talked about and you see signs at airports about financial wellness. You see ads in newspapers. Everybody is talking about financial wellness and despite its growth, at least in marketing terms, workers in the United States are still unwell.

The second thing that I cover is how to identify what financial wellness really means to your workforce. And finally, the third point is how to take advantage of the knowledge, to identify the right financial wellness program that will make the greatest impact on your employee’s wellbeing and your company’s success.

In the last year, there were 2.3 million new millionaires in the US, which is an 11% increase over the previous year. China had 22% increase, Switzerland had 28% increase, Canada had 14% increase. Brazil lost 22% of their millionaires, and apparently that was related to devaluation. One would expect that in this complex year, which is still ongoing, there may be a different picture to paint, but there isn’t. The number of millionaires grew in spades.

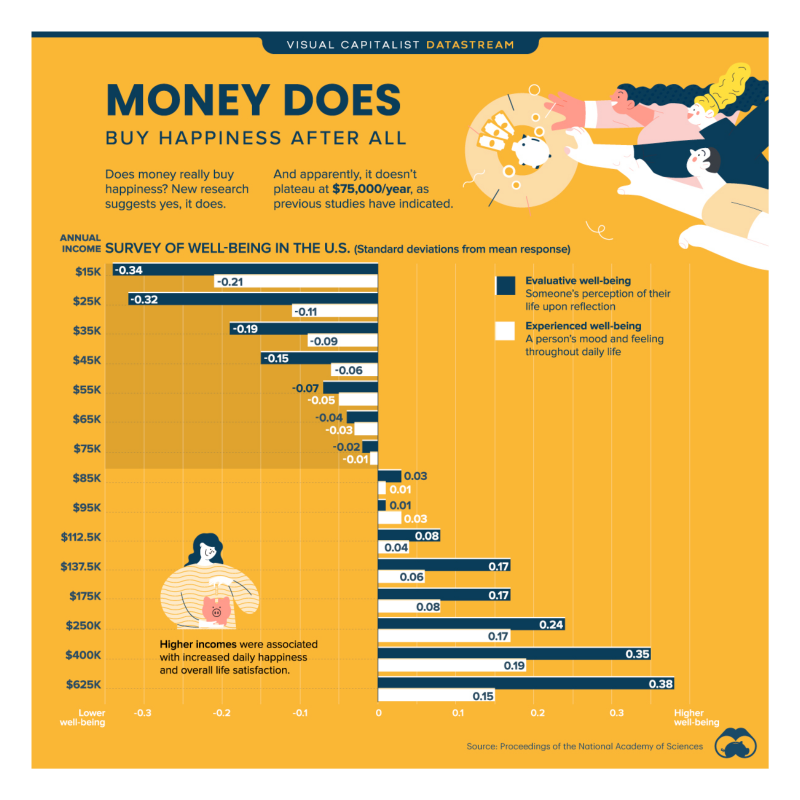

Does money equate to happiness?

This is from the proceedings of National Academy of Sciences, you don’t get more prestigious than that. The biggest study included about 34,000 adults in the US, the median age was 33, and household income was about $85,000. Instead of taking data from the past and asking, “How did you feel in some situation?” they actually gave them a mood tracking app. This was real time, so they expressed their feelings as they felt them.

The question was, “Does money really buy happiness?” Surprisingly, it turns out it does. If you look at the chart, at the $75,000 to $85,000 level, people start saying that they feel happy. Those people who made less than that per year did not feel happy with the mood tracking app. When they were asked, “but why?” they said, “when we have a little more money, we feel comfortable.” 74% said a semblance of control, “We feel in control of our lives.” So this is a very remarkable study, and I wanted this to be a basis as we build this discussion.

Now that we’ve determined that the number of millionaires grew by 11% and money does buy happiness, let’s get into financial wellness.

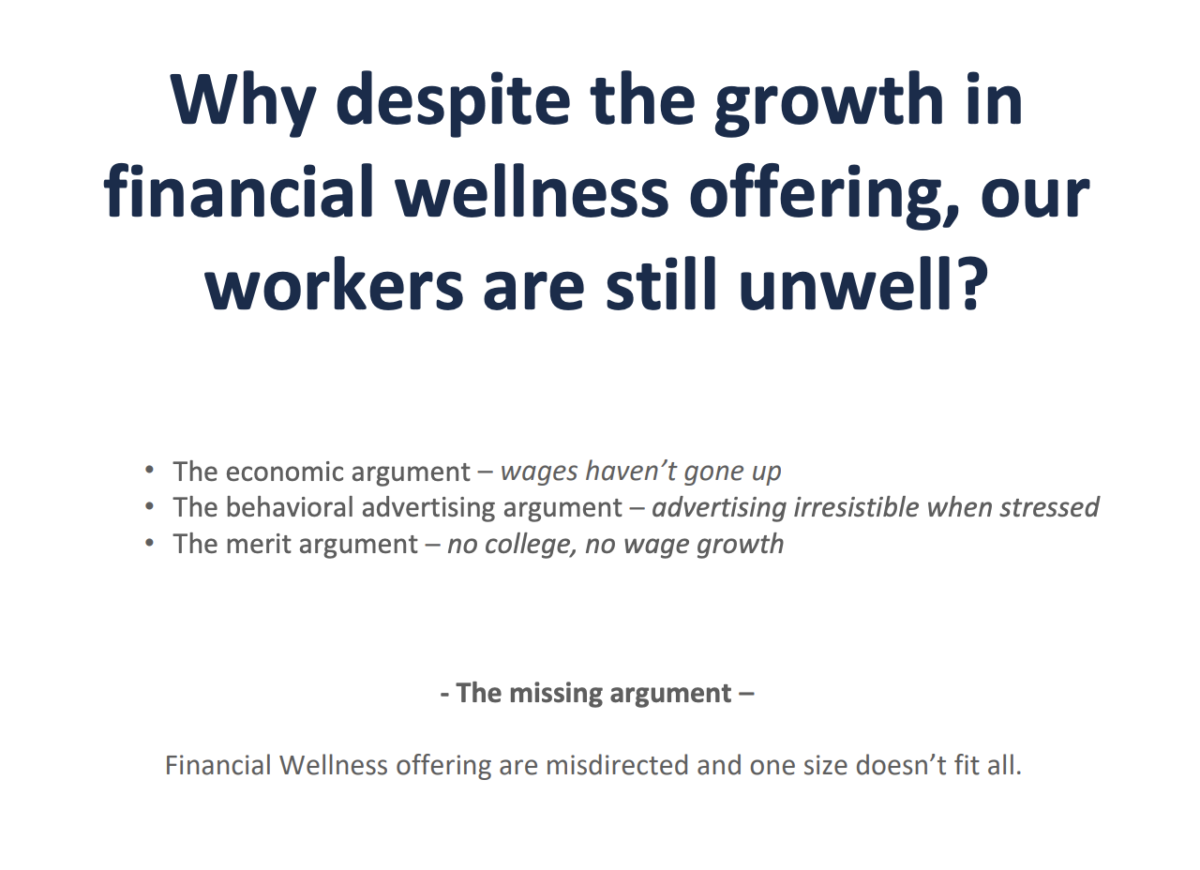

Why despite the growth in financial wellness offering are workers still unwell?

I’ll present to you three different ways to look at it. I’ve taken this approach to give you a foundation or a basis to build an argument in your workforce, in your conversations, when you meet people, when you think about this from the context of human resources.

There is an economic argument. That argument could be people are not paid enough and so on and so forth. There is also the behavioral advertising argument, that advertising has become so slick and sophisticated that it is able to make people make buying decisions when they don’t necessary need to buy. And then there is the merit argument, that people who don’t go to college don’t make enough money and they don’t have any wage growth.

And then there’s a missing argument, that are we doing everything right when we talk about financial wellness?

The economic argument

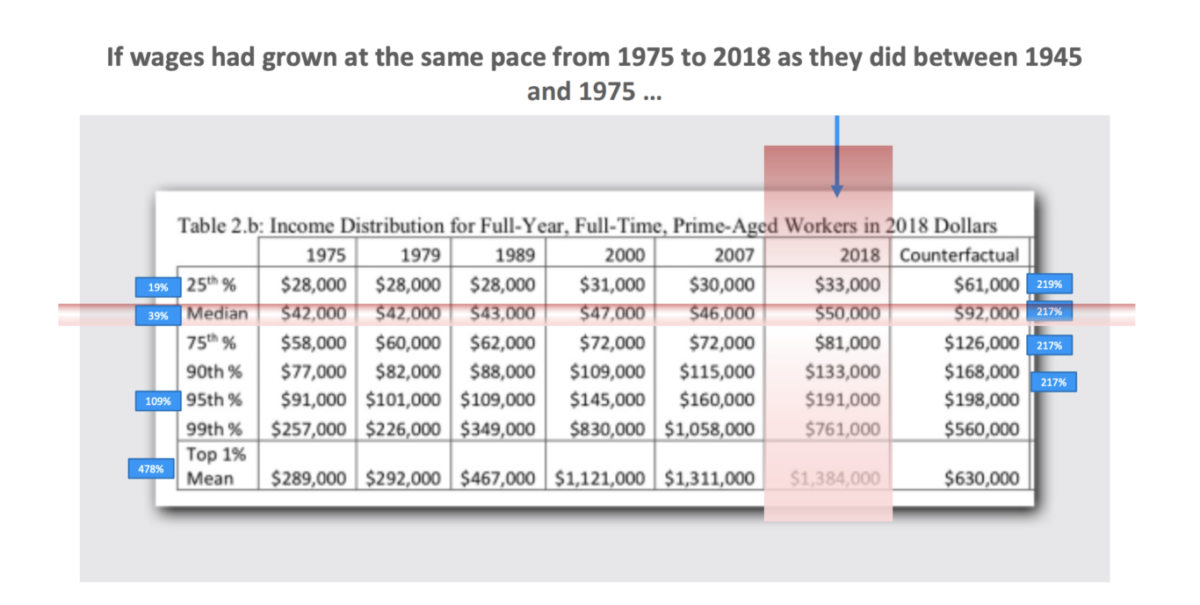

Fast Company did analysis of the study by Rand, which is one of the premier research think tanks. In that study, they asked the question, what would happen if the growth between 1945, which is after the Second World War, to 1975 had occurred from 1975 to now? If the same economic growth had occurred, then what would have happened to salaries at various levels?

The median income in the United States in 2018 was $50,000. The average could be $80,000 or $90,000. When we say average, you could take somebody very tall person with somebody who’s a short person and you could say if one person is 7 ft tall, one person is 5 ft tall, the average would be 6 ft. But that’s not the right way to look at it. You have to look at the median. When you look at the median in 2018, it was $50,000.

If the same growth that occurred from 1945 to 1975 had occurred for all income levels, then their median, the counterfactual, would have been $92,000. So where did $42,000 disappear? If you look at it that way you can see different levels of income. So someone who made $91,000 in 1975 is making $191,000 in 2018. However, someone who was making $42,000 in 1975 is making only $50,000 in 2018, and I don’t think it’s any better in 2020.

This is indicating that a large percent of the US workforce has not grown at all, and the money that they would have or could have made if the growth had been steady in these last three decades as compared to ’45 to ’75, then they would have been at a totally different income level. Why and how and all that is not what I’m discussing. I’m just pointing out to you that this is what happened. Income grew at the top 50% level pretty much linearly. But at the bottom 50% level, there has been a terrible, terrible lack of growth. That also makes financial wellness a very, very important topic.

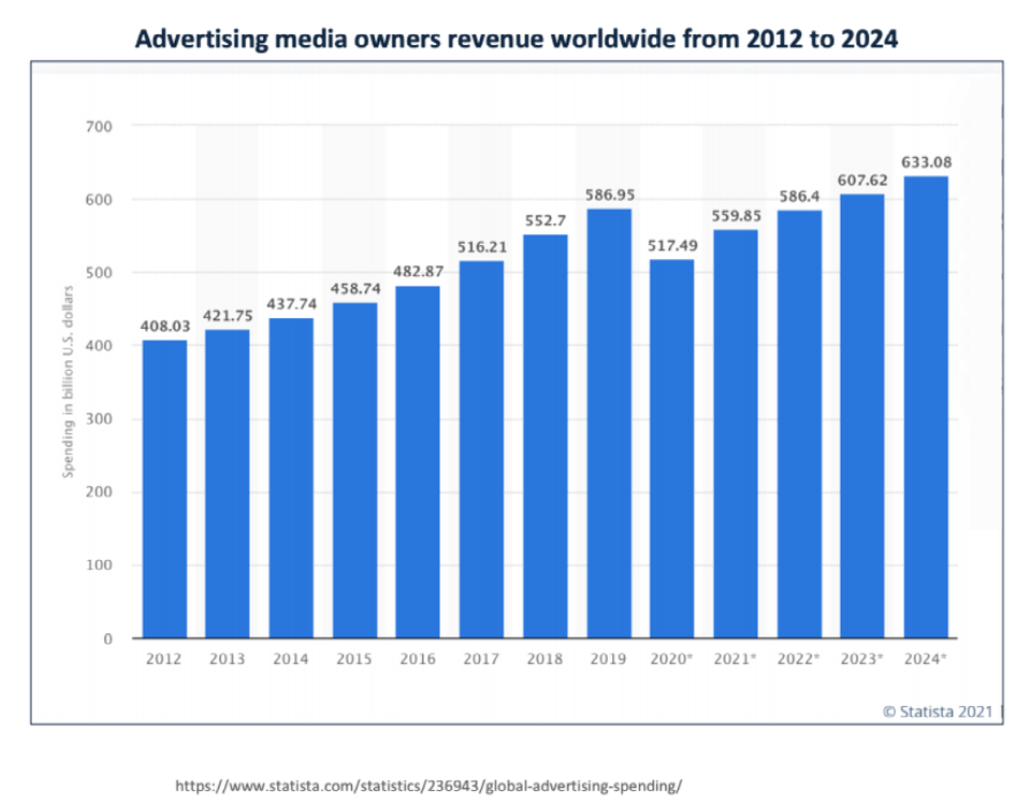

The second argument is the advertising argument.

There’s a relentless growth in advertising and there’s a significant improvement in the quality of how advertising works today, at what time to show an ad, how to show context in ads, and how to make people buy.

Obviously, it works in detrimental ways for people who are financially stressed. Hence, again, the need for financial wellness in some form.

The missing argument. When we talk about financial wellness, what do we really mean?

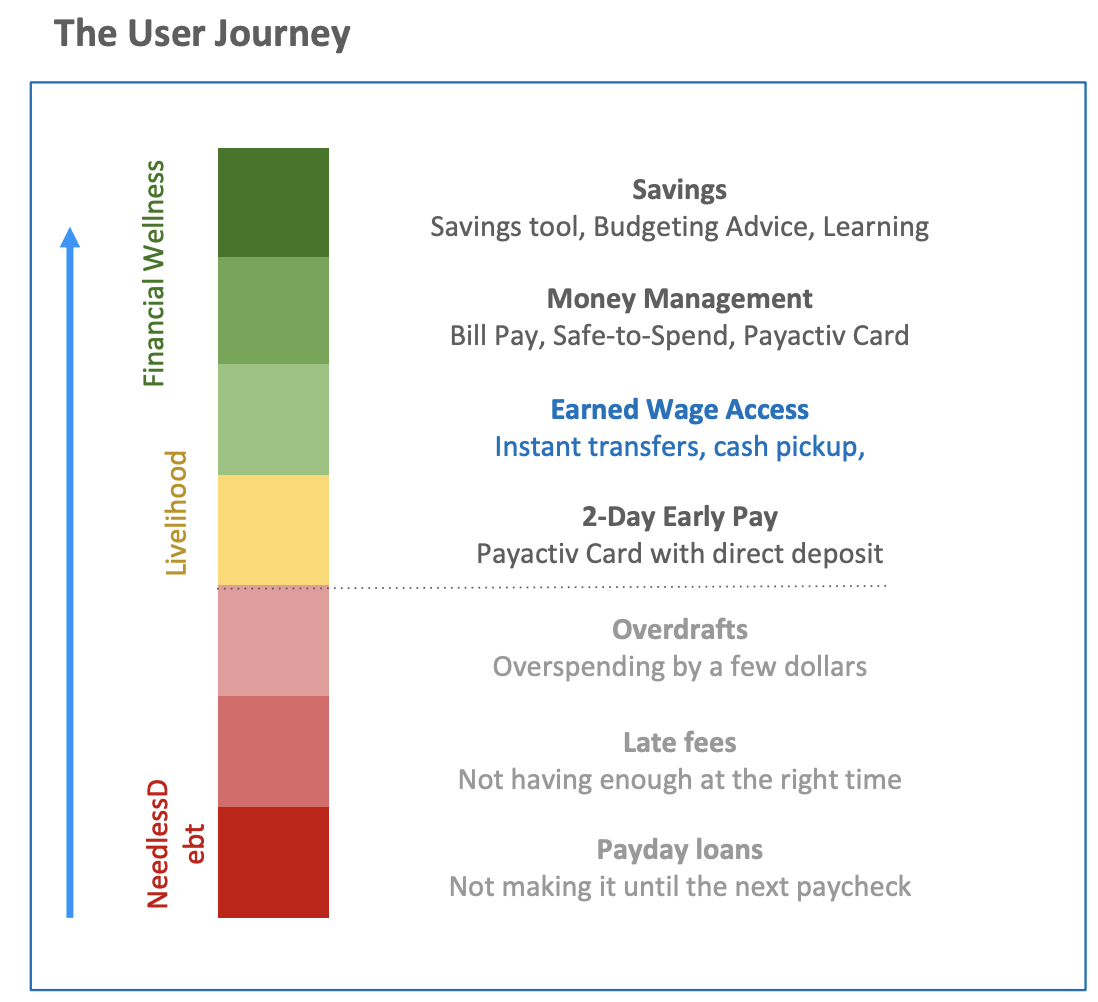

Financial wellness only begins after all livelihood needs are met. We live in a world and a society of haves and have-nots. But there’s another way to look at it, there are those people who are looking for liquidity or just small amounts of money, and then those people who are enjoying compounding, who are investing their money and watching it grow.

In a world divided between people seeking, searching, hunting for liquidity versus people who are enjoying compounding, how do you reconcile the two? The number of people searching for liquidity is growing astronomically. Those people are looking for liquidity because they need food, fuel, or money to drive a car to work. They want to buy various types of insurances to have protection. Thriving only comes after surviving. We can only talk about genuine financial wellness if you want to be practical about it. We can use it as a marketing term all day long, but if you want to be really practical about it, there are people in our country who are looking for food and shelter in most cases. And for them, financial wellness is an aspiration.

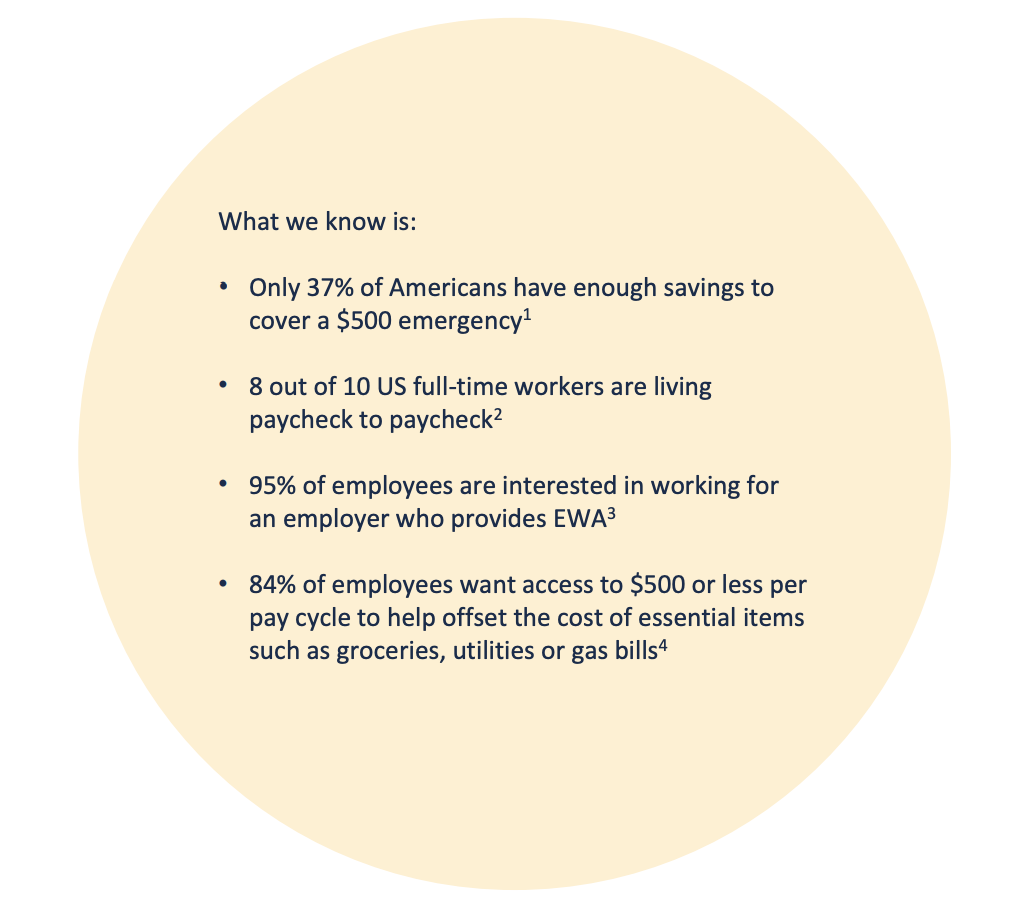

1 https://www.bankrate.com/banking/savings/survey-how-americans-contend-with-unexpected-expenses/

2,3,4 Visa Insights 2019 – Earned Wage Access.pdf

COVID has, of course, been very, very harsh on that segment of society. It has stripped many workers of jobs. So we may be taking the wrong medicine when we talk of financial wellness as this one size fits all. There are subtleties to understanding financial wellness. I won’t belabor on this thing that 37% Americans don’t have enough savings to cover a $500 emergency. This data has been talked about numerous times and you see it in every kind of publication. We also know that over 100 million people in the US, and they could be making $100,000 a year, are living paycheck-to-paycheck.

In March/April 2020 we did a survey to the businesses that we offer our services to, which are related to financial wellness. We asked them, “what are you afraid of?” And they said, “we are afraid of not having money.” They were not afraid of the pandemic. So this is the time we live in, and the missing argument of truly understanding what financial wellness is, what are the subtleties and nuances, because one size doesn’t fit all.

So what is financial wellness?

First of all, financial wellness only begins after livelihood needs are met. I use the word livelihood for a very particular reason, because it means securing basic necessities of life. Food, fuel, auto, shelter, water, all those things are what people are struggling for.

nleys of the world. When they talked about retirement planning, about annuities, about 401(k)s, they were talking about those things. And now we’ve taken that financial wellness word and stretched it to people who are struggling for livelihood. It doesn’t scale that way.

Most people that may need financial wellness today don’t even know what it means. They’re talking about, “How do I get money for gas?” They don’t talk about retirement. This goes back to the question of liquidity versus compounding. Most people are looking for liquidity, just $100 or $200 to make ends meet. So this to me is very, very instructive, that people use terms like relief from financial stress, to be debt free, to have financial freedom. All of these states actually precede planning for retirement. In my decade of talking to businesses, more than 2,000 businesses I’ve talked to, large and small, they always start by saying, “We need to have financial literacy. People don’t know how to save money.” I don’t know what to say often so I finally started saying that to them, that you don’t give a starving person a diet Coke.

All data and research show that financial literacy doesn’t work on adults or works very minimally.

It has to be there, I do not disagree with that, but it doesn’t really do what you think it is going to do. As an entrepreneur, I have actually withdrawn from my 401(k) two times to start companies. These are 20, 25 years ago. You get penalized, but if you’re really hard up in your life, you do end up taking money out of your 401(k). This is something that many employers don’t want to do in their companies because it’s bad for the employee as well.

As I said earlier, one size doesn’t fit all. I think at the center of it all is the employer/employee relationship. We do always say “human resource”, but at the end of the day, humans are not a resource, they are the source. We need to find a way to start a dialogue or discussion about money in workplaces.

At the heart of it, the employer/employee relationship. We have to figure out a way to create a two-way communication, to know what your employees are going through. We have to start listening. Do we know if our employees are struggling each day? Have we just made a blanket statement that, “I will not accept that they could have a life challenge? They just messed up and they want money.” We have to get over that reasoning. These are some the things that when you listen to employees, when you show understanding and compassion, you can actually build data for your company, for the neighborhoods where your company serves. Because the zip code matters, the rents matter, the distance from work they have to drive matters. If there’s no public transportation, they will have to take an Uber if their car breaks down, or some other type of transportation. They may not have money, and that may just mess up the entire day. It degrades self-esteem, it destroys the self-respect that you have, the dignity that you have. All those things then come to work like absenteeism, and presentism.

You also need to know if there are payday lenders in neighborhoods, and now payday lenders have all migrated to the online world, right? They’re on the internet. So they’re on everybody’s phone and your workers are facing them. Their aspiration is not financial wellness as you think of it, but something different.

So where are your workers turning for help?

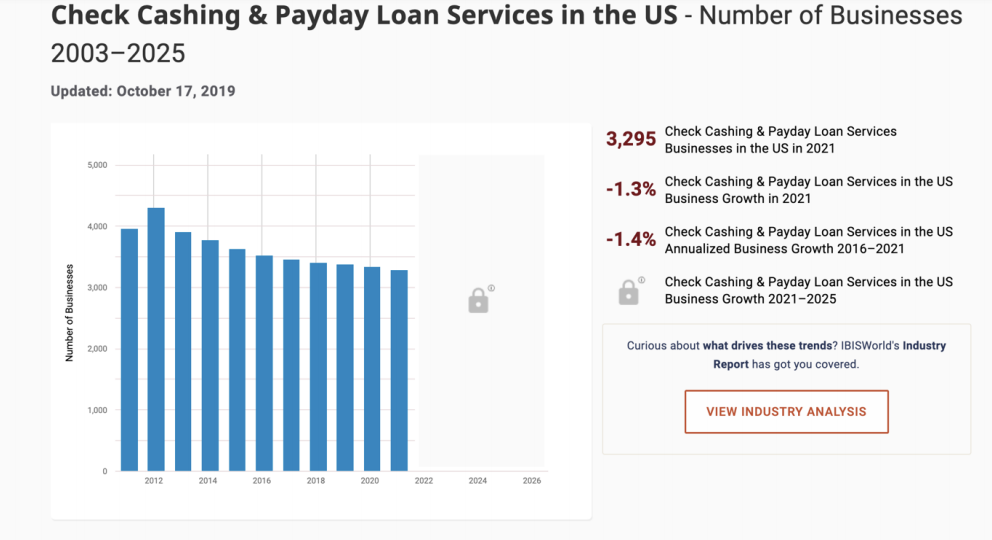

Just to frame it for you for a moment, there are $200 billion paid in fees or interest income every year for the alternative financial services industry. This is money paid by people for challenges of liquidity who need a small amount of money. Now, who is getting the $200 billion? $35 billion every year are paid in overdraft fees. People will write a check, get hit by the overdraft, and then deal with the consequences. An overdraft can be $35. That’s a $35 billion industry.

Another big one is in many states in the US where payday lending is banned, auto title loan business is not banned. The single biggest possession for most people is a $3,000 to $5,000 car. When they need $200, they end up using the title of that $5,000 car for $1,000 in loan, and the interest rates for that are exorbitant. Then there is a whole industry which people have not really quantified yet, and I spent some time looking at that industry, it is the late fees that people pay.

I did this experiment about three years ago where I stopped paying every single bill to see what happens with my utility bill, with my T-Mobile bill, with my Verizon bill, with all the bills, and in three months, I had destroyed all my status and stature. Literally, you can do that, and that is what happens to millions of people.

So where are users turning to today? Well, of course there are the check cashers, but there is also a whole new class of industry that has popped up, the fin-tech industry. There are dozens of these products, and your workers are relying on them. Your workers are reliant whether they call themselves a digital wallet or a challenger bank. Not all of them are interested in helping you live in your day-to-day and grow for whatever you need to plan.

They are all there to generate transactions, because as you can probably surmise, in America today, over 100 million people don’t have money to create deposits, because they don’t have savings. That’s the consequence of paycheck-to-paycheck, that means you don’t have much money to deposit in the bank. So you are automatically uninteresting to the bank system. Banking systems rely on deposits. So what do they have those 100 million people? They have transactions, everyone wants those transactions, from Visa and MasterCard on one end to all the businesses in the middle, the entire fin-tech payment ecosystem.

This is how these individuals are monetized, and that is where leaders in HR have to think about, are my workers before monetized? Can I institute an employer-sponsored program which will be effective and which will co-exist with the products that they will use inevitably?

Which financial wellness programs make the greatest impact on your employees and your company’s success?

A good solution is the one that allows you to deal with your day-to-day and sets you up for your short-term needs and also prepares you through its own structure how much to spend, how much to save, how much to pay for services. In this day and age where almost everything has been redesigned for the social collaboration and communication mechanisms, why is it that financial products are not designed that way? So that the education is embedded in it, then nudges their behavioral stuff.

How do you take a user from surviving to thriving?

I think the key thing that we have found in our work is telling users what is safe to spend, smart spending, analyses of spending, and do it naturally. As they spend, they find out, “Oh, I could have done better”. Also, educate them on what is safe to save. As all of you know, there are bragging rights toward spending, there are no bragging rights toward saving. Nobody posts their savings account’s picture on Facebook, but the new sofa, the vacation, they all go on Facebook because there are bragging rights there.

My company has invented something about nine years ago, and we called it Earned Wage Access, which allows people to access what they’ve earned as they earn it, with a guardrail built in it that they can get half of what they’ve earned, because the remaining half is rent and the big ticket items. That is how we started a whole category in this industry called Earned Wage Access. I’m very particular, I called it Earned Wage Access because it is already earned, so it’s not a loan. Using that approach, we learnt a lot.

Almost nine years ago when I first saw a company where I went to the employer and I said to them that, “Your employees look for advances and go to pay their lenders. Would you let me provide a service to your workforce, where when they’ve earned $100 they can get $50, and I give them $50 and you reimburse me at the end of the pay cycle, weekly, bi-weekly, monthly, whatever?” The employer scoffed initially but then they said, “Yeah, it’s an interesting idea. We give advances, and we’re very worried when we give advances because we don’t know if it’s legal and all that and are we distinguishing between who to give an advance to and so forth.” And that was that day, 2013, that this idea was born.

Earned Wage Access was the tool that we set, which allows you to solve the problem of liquidity without letting you get into trouble. So if a bill comes in for $50 and you need $50, you don’t need to go and borrow it from somebody, you obviously don’t have a credit card, you shouldn’t take a payday loan, and you shouldn’t be stressing about it, because you’ve already earned the money. But it’s sitting with the employer, it was going to be paid to you two weeks later.

In 2017, we were deployed in Walmart, which is the world’s largest employer. It’s amazing to see the impact on the lives of people when you let them access what is already theirs. I know there are lot of views and thoughts that will come to your mind, “How can it work?” The answer to you is, when people have earned their wages, they’re earning it every single day.

Everything else in the world is real time, right?

We pay our landlords in advance. We pay our vendors upon delivery or set terms. As soon as I buy the latte at Starbucks I give them money for that, but the barista, the person behind the counter waits two weeks to get paid. Why? There is no logic. That is the one who’s suffering the most. If they can access 20%, 30% of the money they’ve already earned, they won’t get into the worst situation, the needless debt situation. I’m not questioning anything else, I’m saying debt that is needlessly caused by late fees and penalties is not necessary. We can solve it by giving Earned Wage Access or timely access to earned wages. That is the sort of financial wellness foundation that we launched and that’s what I do. The results across companies are astounding.

These are some of the ways that many of you who are thinking about financial wellness can institute it. My company has 10 years of experience. I live and breathe this every single day. This is my purpose. I do not know what we will do in the next two, three, four years, but every day we’re figuring way to find tools and technics for how to help workers at all levels, young, old, low income, higher income, to find ways to help them to achieve financial wellness. But until then, my belief is that there are millions of people who are struggling for livelihood. First, let’s also focus on them. These are the people who are surviving, and then we can help them get to thriving.

Q&A

“How can it be implemented in a smaller environment?”

We work with companies which are the size of Walmart and work with companies which have 5, 10, 20, 50. Payactiv has access to their hourly data, time and attendance data. We put up the money, we give the money to the employee, and you as an employer has to reimburse us. There are also options for people to not have to pay anything if they use our card. So in our model they can pay their bills right from the app. They can start a savings program with a few key strokes. And they can do spend analysis, what they’re purchasing and so forth because there’s a card attached to it. They can also link another bank account, their savings account and they can add it all together.

We work in many school districts, we work in warehouses, call centers, hundreds and hundreds of senior living centers and hospitals and very, very large employers in various categories in healthcare, hospitality, restaurants, and so forth.

“How do you achieve a balanced program that encourages better financial decisions?”

We operate with this assumption that when people have access to money, they will somehow misuse it. It may be true in some cases, but what really happens is they think of it like bingeing versus grazing. If you’re starved for the whole day and you are given a meal at the end of the day, you will end up eating 2,000-3,000 calories at the end of the day, because by that time you are in the starvation mode. But if you had access to small amounts of food during the course of the day, this is what happens in good financial wellness. Do not let the individual get into the equivalent of a starvation mode. Instead of worrying about whether they’ll misuse it, let them access what they’ve earned, let them live the life that they have earned, and they will know how to manage it.

Because who owes whom here? The employer owes the employee or the employee owes employer?

“Are you working with schools/colleges?”

Yes, we do. The school/college issue is very interesting. It’s a nine month work year. What happens to the janitor in the remaining three months when the kids are not at school? What is the janitor doing? How is the janitor earning their money?

“What is a good strategy to use when discussing helping employees with the C-suite?”

When I started this, I call it almost a purpose-driven movement, 10 years ago, I went to the C-suite and I found them to be the most thoughtful and welcoming. There I found it easiest to understand the three things they care about. Remember a business is built on the shoulders of its employees. Any data which shows that your employee and workforce is doing well means that your customers are also going to do well.

Businesses live and die on the altar of their customer and they want happy employees, use these three arguments, that these three expenses without an invoice, recruitment, retention and engagement, can be impacted significantly, that’s one. Number two, in the new class of financial wellness services like what we do, there is no change in treasury cost. So the salary that is going to be paid every two weeks continues to get paid every two weeks. No change, because there’s a third party which is actually moving the money back and forth. Third, it doesn’t cost anything to the employee, because you’re comparing $35 payday loan versus a $1 fee, if at all. These are the things that should be mentioned to a C-suite. It will improve recruitment, retention, and engagement. It will also improve the overall customer service, customer experience because employees would be happy.

For additional resources, check out Payactiv Insights.

Get Payactiv for your business

Learn how thousands of companies have improved their retention, recruitment, and engagement by offering Payactiv.

Request a Demo

Related Articles

A car breakdown, an unexpected medical bill, and a broken appliance We all know...

You spoke, we listened Thank you Our app is a response to the pressing needs of...

Payactiv's zero-cost benefit creates opportunities for workers to fully engage...